In 2014, TASC published A Defence of Taxation. Its argument in favour of progressive alternatives to reducing public services through tax cuts remains as salient as ever, and it is an appropriate topic to revisit on the 25th anniversary of TASC.

The context has changed, but Ireland’s tax system is still unstable and unsustainable, despite several years of strong economic activity and extremely high receipts from corporation tax. Successive governments have been warned by IFAC and others that over-reliance on taxes from a handful of multinationals is highly risky. While the government is saving some of that money, IFAC and others say that it isn’t enough and the recent trend is for more spending and less saving of the windfall, overheating the economy when it isn’t needed and not leaving enough for the next downturn.

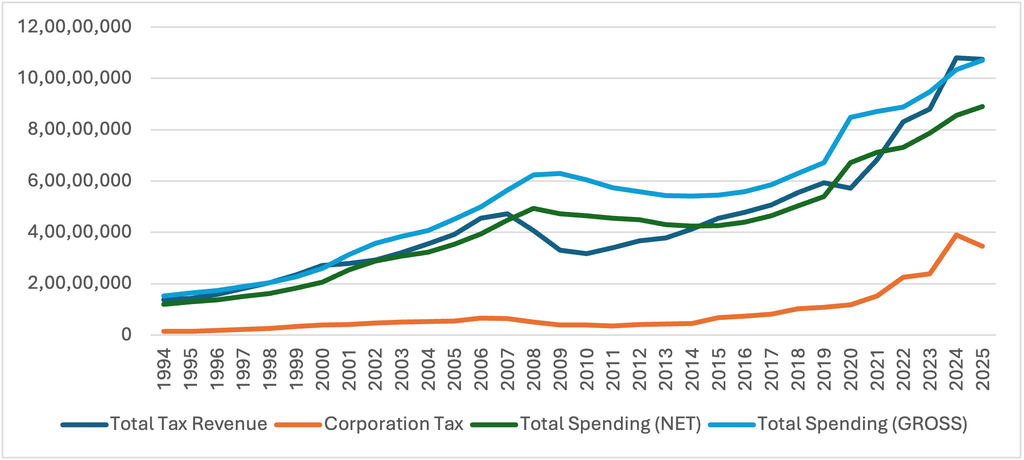

Ireland’s Highly Risky Tax Model

The following chart puts this into perspective. In 1994, corporation tax receipts were 10.5% of all tax revenue, already up 250% from 4.0% in 1984. The 12.5 per cent rate of corporation tax was announced in 1997 and implemented in the last years of the 1990s. By 2025, corporation tax represents 32.3% of all tax revenue. If you factor in VAT and income taxes paid by the large multinationals, more than half of all tax revenue could be coming from fewer than ten foreign-owned global firms, mostly American.

Figure 1. Public Spending and Tax Revenue €000s, 1994-2025 (DPER/Finance Databank)

On the back of this windfall, there has been a bonanza of public spending, up from €12 billion (net) in 1994 to €89 billion in 2025. The recent trend has been one of rapid acceleration of spending. In the last ten years, public spending doubled, up from €44 billion in 2016. Granted, there was high inflation in this period, but the sustainability of this spending is being seriously questioned by many analysts outside the government, and privately by some civil servants within the system, who fear that the politicians have (once again) lost their grip on the public purse. Those with least, who rely on social protection and public services most, will be hardest hit if multinationals simply declare their profits elsewhere, as Trump’s USA may well pressure them to do.

It makes sense to also look at gross public spending to indicate the level of risk, as much of the gap between gross and net public spending is covered by social insurance payments (PRSI), and once again a few multinationals are paying a large share of this, even though the associated social protection spending is not going towards their workers. In other words, if a few multinationals left, we would lose the PRSI receipts but still have committed to the related social protection spending.

The simple conclusion from this is that neither Fianna Fáil nor Fine Gael have become truly social democratic over the last decade. They are willing to spend money, but not to build a robust tax system. Their fiscal policy is populist and reckless, rather than social democratic.

Taxes as Collective Purchase

Back in 2014, in A Defence of Taxation, our three contributions were a description of Ireland’s level of taxation, an analysis of the economic effects of taxation, and proposals for alternative tax reforms from what was being considered at that time, which we argued would have made more people materially better off than from tax cuts.

Before updating the analysis of these points, I want to draw attention to one of the most obvious aspects of tax, which is nonetheless overlooked in the media commentary: we pay taxes to collectively purchase goods and services because this is often more efficient than paying for them individually. We also pay taxes for other reasons, such as redistribution, but the bulk of taxation is to pay for goods and services that we want for ourselves. A truly social democratic tax system – such as exists in the Nordic countries – is based on collective purchase mechanisms and is highly transactional, as will be outlined below.

Here are six useful (and sometimes overlapping) ways of thinking about taxation:

- Transactionality

- Deferral

- Quasi-insurance

- Debt repayment

- Redistribution

- Incentives

The first four points relate to the collective purchase of goods and services. Just like in market transactions, public spending offers multiple different ways to pay, including a direct transaction or deferral, quasi-insurance or borrowing (combined with the later repayment of public debt).

Transactionality describes taxation as a purchase: X pays taxes to receive Y goods or services. For example, the funding of public goods through taxation, such as defence, public lighting or maintaining the road network, is fundamentally a transactional relationship. Most people are paying taxes towards something that they will use or benefit from. We might pay collectively because there isn’t a practical way to impose pay-per-use, such as for street lighting or defence, or we might pay collectively because the state provides a service as a monopoly—such as much of healthcare—and a private monopoly would cost us more than a public one. There are also hybrid arrangements where tax-funded services also levy a user charge or fee, such as the €100 fee to access hospital accident and emergency (A&E) departments (but technically that isn’t taxation but appropriations-in-aid that gives us the difference between gross and net public spending). This particular fee may not even be motivated by revenue generation as much as by reducing demand for A&E by pushing less urgent cases to cheaper primary care services.

Deferral means use now, pay later. An example of deferral is education. We all can receive an education from the state, including early years, primary, secondary and/or third level education, and we pay for this in arrears by funding the next generation’s education. There are different rationales for this. We could consider that our parents’ generation paid for us, so we pay for the next generation as part of a social contract. Or we might simply consider that the state funded our education in advance, partially as an investment, and we pay that investment through our taxes. Alternatively, one could simply describe education spending as transactional, with parents paying taxes as a more efficient mechanism to fund education than private fees. Of course, through hybrid arrangements and ‘voluntary contributions’ some parents may pay fees in addition to taxes, and those who opt for wholly private education may not directly benefit from the state’s investment. Other examples of deferral include paying for roads, healthcare and other services we used as children or as recently arrived migrants.

Quasi-insurance is a way of thinking about situations when we pay taxes towards services we hope we will never need to use, such as the fire brigade, hospital emergency departments or unemployment benefits. No one doubts that they are receiving a valuable service when they pay for home insurance, but they hope they won’t be affected by a fire or flood. Public services are funded by ‘quasi’ insurance because it isn’t a conventional insurance contract, but it simply does a similar thing as insurance. Social insurance in Ireland is a misnomer for this reason, as it isn’t really insurance but just another form of income tax combined with a payroll tax for employers. Taxes that pay for healthcare, social care, social housing and social protection payments can all be understood to be quasi-insurance. Attempts have been made to fund public services through actual insurance schemes, like the Netherlands experiment with mandatory health insurance, but taxation functioning as quasi-insurance is far more common.

Another example of use now, pay later, is the state’s ability to borrow money to provide services today, while future generations repay the public debt and associated interest payments. In this case, we pay taxes on the debt that we (and past generations) have incurred. In principle, borrowing should only be used for capital investment that will ‘pay for itself’ through expanding economic production, but in reality debt is incurred for a variety of reasons, including to pay for day-to-day spending in a way that imposes a direct cost on future generations for services that are received today.

All of the above can be understood as transactions between taxpayers and the state for goods and services, and a social democratic defence of taxation can and should be based on the argument that if you want high quality public services and assurance against bad luck, this is something that you should personally be willing to pay towards. Economies of scale and state-run monopolies make collective purchase cheaper than relying on markets and paying individually for the same services, and some public goods (like street lighting or defence) simply must be funded collectively.

Another dimension of taxation is redistribution. There is a mistaken view that distribution is the main role of taxation, but this aspect of taxation tends to be over-hyped by opponents of public services or state interventions. The mechanism for redistribution is not as simple as saying taxes that go on social housing or social welfare are automatically redistributive. Some part of those taxes are better understood as quasi-insurance. A person may have a secure job, but they are still entitled to social protection should they ever need it, so they cannot claim that all their taxes that go on social protection are purely redistributive. Nonetheless, there is a redistributive element to most taxation because those with higher incomes or greater wealth pay more, while those with less of both, pay less in taxation. This is not always a proportional thing, as Dr Micheál Collins has demonstrated, those on the lowest incomes often pay as much tax (such as VAT) as a proportion of their incomes as those on higher incomes, but it is true in terms of amount paid. Overall, the extent of redistribution in a given tax system is not straightforward to measure as we don’t have full data on how much taxes people pay (including indirect taxes) and we don’t have anything like an estimate for the cost of the public services that each individual or household receives over their lifetime.

Another aspect of taxation is incentive, often to correct market failures. The plastic bag levy, landfill levy, tobacco excise and carbon taxes are all designed primarily to change behaviour rather than to raise revenue into the long-term. Tax breaks or lower tax rates, including the zero VAT rate, are also designed to promote policy outcomes rather than maximise revenue. Some taxes, such as Local Property Tax, also have useful policy outcomes, such as suppressing house prices (although Ireland’s low levels of LPT hasn’t had much effect).

A Defence of Taxation Revisited

As a percentage of GDP, Ireland’s taxation is fourth lowest in the OECD. There is a strong argument to not use GDP when examining public spending, but that argument isn’t as strong when it comes to taxation. GDP – including paper transactions by multinationals – represents economic activity passing through Ireland, which we could tax. The fact that we don’t is what attracts multinationals to base themselves in Ireland, which is why we end up with the high flows of taxation shown earlier. But the untaxed economic activity represents tax lost to the EU as a whole, so it is not without a wider social, economic and political costs.

When Ireland is compared to OECD countries, our level of taxation (as %GNI* rather than GDP) is lower than many EU countries (especially those with stronger welfare states) but is higher than most non-EU OECD members. In particular, Ireland’s ‘tax wedge’ (personal taxes) is slightly above the OECD average. What’s unusual is that personal taxes are highly skewed in Ireland, with low to middle income earners paying less and higher income earners paying more, which is the main redistributive part of the tax system.

As a whole, Ireland’s tax system has the economic effect of encouraging foreign direct investment, heavily subsidising certain private sector purchases for higher earners (like private pensions and health insurance), and fuelling a higher-than-average cost of living as Irish workers tend to have more cash, but also more out-of-pocket expenses for costs that would be free-of-charge (purchased collectively) in other EU states. The area of lowest taxation in Ireland is social insurance, with employers’ contributions far below western European levels. However, social insurance is linked to employment, so raising PRSI rapidly would probably have a significant and negative effect on employment levels.

Any serious attempt to make Ireland a social democratic state would need to reduce or eliminate tax breaks, increase social insurance and also increase the share of taxes paid by low and middle income workers. It’s not an easy manifesto to sell, but the core principle of collective purchase should be front and centre in explaining why Irish people can’t put all the heavy lifting onto multinational corporations if we want high quality public services and robust state pensions, especially as our population ages. One way to sweeten a move towards higher personal taxes for middle incomes would be to foster higher levels of wage growth in the economy too.

The Nordics have achieved their high-taxes-for-excellent-services trade-off by raising a large proportion of taxes locally and also having a very high level of transparency. People can see where their money goes in close proximity to where they live. Ireland’s highly centralised approach to tax and spending would also need to change if we want to become a social democratic country.

Dr Nat O'Connor @natpolicy

Dr Nat O’Connor is Assistant Professor of Social Policy at UCD, a fellow of the UCD Geary Institute for Public Policy and former Director of TASC. Nat also previously worked at Age Action, the Labour Party, Ulster University and the Homeless Agency. You can find him on LinkedIn (natoconnor) and TwitterX @natpolicy.

Share: