Jim Stewart: The announced takeover by Pfizer of Allergan and consequent redomicile of Pfizer to Ireland has attracted enormous international media interest. Much of this comment is critical of both Pfizer and Ireland. This blog considers one aspect of Pfizer and MNE tax strategies, that is switching profits away from or to a tax jurisdiction (Tax Diversion). A further blog tomorrow will discuss inversions as a tax strategy, and some possible implications of the Pfizer transaction.

Diversions as a Tax Strategy

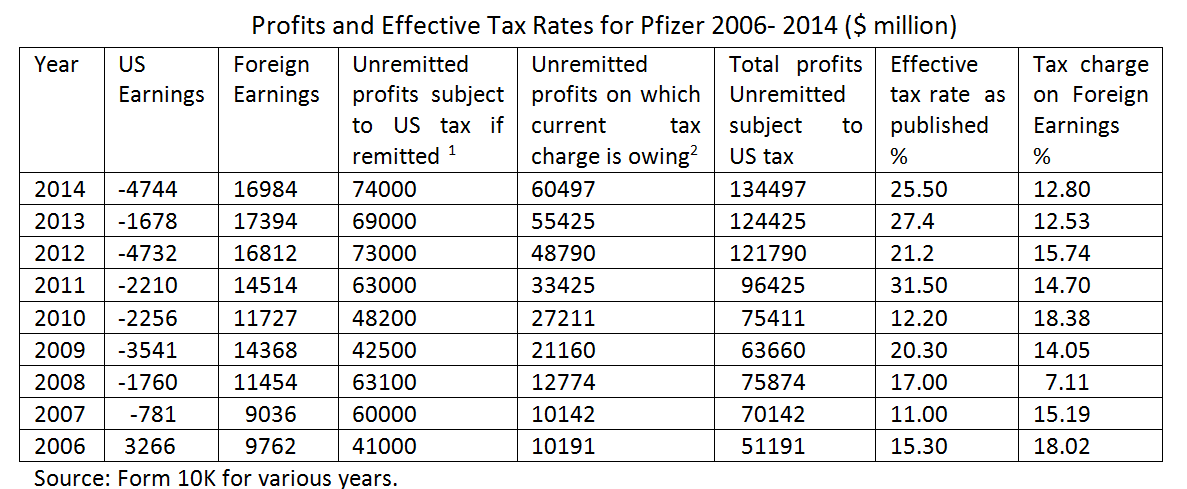

Multinational Enterprise (MNE) corporate tax strategies are complex. MNEs may switch profits both away from a tax jurisdiction or to a tax jurisdiction. Take the case of Pfizer. Since 2006 Pfizer has declared a loss in the US but a profit on its overseas operations, resulting in an overall group profit (see Table 1). Thus foreign profits of Pfizer are large, as are unremitted foreign earnings which have grown from $51.1 billion in 2006 to $134.5 billion in 2014 . At the same time between 36 and 53% of sales arose in the US during the same time period.

Counterintuitively most tax is paid in the US. Table 1 shows that the effective tax rate on foreign earnings (defined as foreign tax paid/foreign earnings) is generally less than half that of the group as a whole (Table 1). If remitted to the US these profits would be subject to substantial extra tax because they have been taxed at a lower rate than the standard tax rate in the US of 35%.

|

| Table 1 |

Pfizer is an extreme example but many US MNE’s earn more profits abroad than in the US but pay less tax abroad than in the US. Thus the greater the proportion of profits earned and retained abroad the lower the tax rate.

An important reason for the surge in corporate tax payment in Ireland is the tax strategy pursued by MNE’s, that is a policy of ‘profit switching transfer pricing’ - diverting profits to Ireland to avail of a very favorable tax regime. Transfer pricing decisions have long distorted aggregate economic data for Ireland, for example a large balance of trade surplus, but negative or low current account balance because of profit repatriations. GDP is thus consistently larger than GNP. Value added per employee in sectors dominated by MNE’s – pharmaceuticals and ICT services is much larger than that for sectors dominated by indigenous firms. Data for 2013 shows that Ireland is the largest single exporter of ICT services and accounts for 12.8% of world exports compared with for example, the US which accounts for 8.1% .

Recent written parliamentary answers have shown the effect of large profits by MNE’s in Ireland on corporate tax receipts. Over 80% of corporate tax payments for 2014 and for 2015 (to October) came from MNE’s (written Parliamentary answer 39980/15) of which pharmaceuticals and ICT (information and communication technologies) sectors are the most significant. Ten MNE groups account for more than one third of corporation tax receipts (written Parliamentary answer 40399/15), and these companies account for over €1 billion of unanticipated corporate tax receipts (written Parliamentary answer 40399/15). Overall these 10 companies could account for over €2.5 billion of corporate tax receipts for 2015. Three of the top 10 corporate tax payers are likely to be Pfizer, Microsoft and Apple. (for Apple see Niall MacSuibhne).

Taxes on corporate income in Ireland as a proportion of total tax revenues (8.4%) are thus higher than for many other countries, such as Germany (4.9%), for 2013, (Source OECD Revenue Statistics for 2015). Using Revenue Commissioners data this ratio for 2014 amounted to 11.2% and is likely to be higher still for 2015. Because profits may be switched to low tax countries, those countries with the most favorable tax regime may be most dependent on corporate tax receipts.

For example, Luxembourg has the highest proportion of taxes on corporate income as a percentage of total tax revenues in the EU at 12.4%. Corporate tax payments in Ireland thus become a function of the amount of profits ‘pushed through’ - a form of transit tax.

Prof James Stewart is a member of TASC's Economists' Network. This is Part 1 of a blog on Inversions and Diversions. Part 2 is available here:

http://www.progressive-economy.ie/2015/12/inversions-as-tax-strategy-implications.html

Notes for Table 1

(1). The tax status of these unremitted earnings is described in Form 10K as follows:- “As of December 31, 2014, we have not made a US tax provision on approximately $74.0 billion of unremitted earnings of our international subsidiaries. As these earnings are intended to be indefinitely reinvested overseas, the determination of a hypothetical unrecognized deferred tax liability as of December 31, 2014, is not practicable (source Form 10K, 2014, p. 81

(2). Form 10K 2014 (p. 81) shows the tax liability due on unremitted earnings, “that will not be indefinitely reinvested overseas”. The total unremitted earnings are calculated as tax liabilities on foreign earnings grossed up by the tax rate (35%).

Prof Jim Stewart

Dr Jim Stewart is Adjunct Associate Professor at Trinity College Dublin. His research interests include Corporate Finance and Taxation, Pension Funds and financial products, Financial Systems and Economic Development.

He is widely published and his titles include Mutuals and Alternative Banking: A Solution to the Financial and Economic Crisis in Ireland (2013), Choosing Your Future: How to Reform Ireland's Pension System (co-author, 2007) and For Richer, For Poorer: An Investigation of the Irish pension system (2005).

Share: