As AE is a funded scheme, the accumulated lump sum and future pension payments are a direct function of contributions and the return on these contributions net of costs. These returns are subject to considerable uncertainty and hence risk.

Recent bank failures and volatility in financial markets have underlined risk associated funded pension schemes.

The failure of SVB Bank has been attributed to a rise in long term government debt yields and an associated fall in bond prices ((https://edition.cnn.com/2023/03/13/investing/silicon-valley-bank-collapse-explained/index.html).

Although other bank failures such as Credit Suisse, have not been attributed to bond write downs, rising interest rates is a common theme (https://www.ft.com/content/cd76f8d4-1b10-48a3-a8ee-06925f32c0ce).

One estimate that the market value of Government debt held by US banks for March 2023 is $2000 billion lower than the values reported in their accounts. This has implications for bank liquidity coupled with uninsured deposits (see Jiang et al at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4387676).In

In Ireland commercial property fell 14% in the year to September 2023 (Central Bank Financial Stability Review 2023, p. 19).

A fall in bond prices has considerable implications for pension portfolios. The fall in values has led to large capital losses (on a mark to market basis). Real yields are negative with implications for pension payments.

A fall in assets is not necessarily linked to pension fund solvency. However if liabilities (future pension payments) are directly linked to likely higher future pay and pension pay outs, as may be the case with some DB schemes.

Rather a fall in bond prices resulting in capital losses may be associated with a increase in solvency as liabilities are discounted at a higher rate as shown in Table (2)..

Table (2) shows a fall in asset values for two pension schemes (Dairygold Co-op Society and Aurora Co-op Society) most of whose assets and liabilities are in Ireland.

Table (2)

Asset Declines and the Actuarial Surplus: Some Examples (€ million)

|

|

|

|

Dairygold Co-op | 2022 | 2021 | 2020 |

Scheme assets | 234.534 | 300.397 | 282.18 |

Bonds | 196.619 | 204.832 | 169.501 |

Scheme Liabilities | 179.815 | 261.861 | 251.773 |

Surplus | 54.719 | 38.536 | 30.407 |

Discount rate | 4.1 | 1.3 | 1.35 |

|

|

|

|

Aurora Co-op Society |

|

|

|

Scheme assets | 42.166 | 58.097 |

|

Bonds |

|

|

|

Scheme Liabilities | 38.470 | 57.545 |

|

Surplus | 3.234 | 0.48 |

|

Discount rate | 3.75 | 1.35 |

|

Source Annual report and Accounts for Dairygold Co-op Society and Aurora Co-op Society

Changes in end of year asset values may also reflect asset switching during the year, net sales of equities and net purchases of bonds.

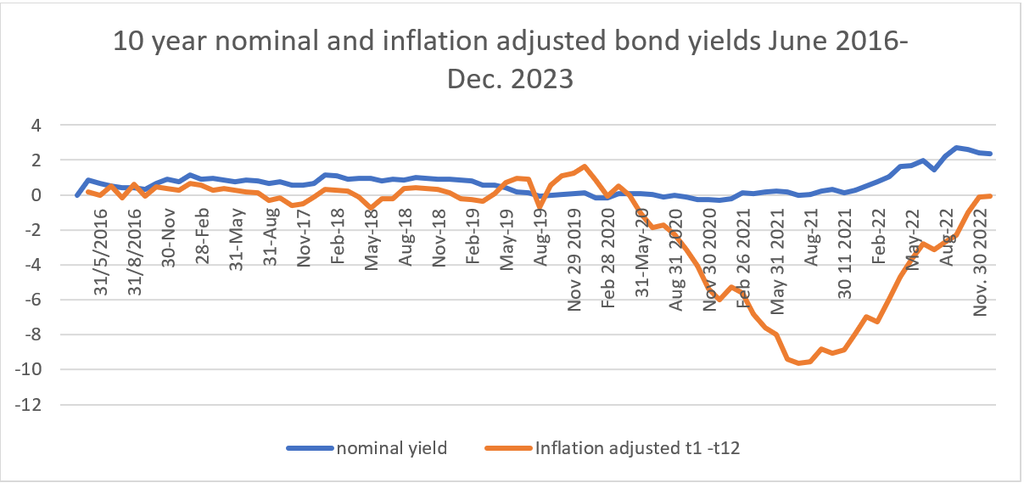

Apart from a fall in asset value, real interest income on bonds has also fallen as shown in the graph below. The graph shows that for a three year period from oct 2020 to Oct 2023, yields were negative. The one year yield for July 2021 was -9.6%.

Data Source for bond yields:- Investing.Com.

The Bond yield used is that quoted for the last trading day in each month. The rate of inflation is from Eurostat release HICP – monthly data (annual rate of change). The inflation adjusted yield is calculated over a 12 month period as yield in time period t - rate of inflation over the following twelve month period. This is a measure of the return to a bond purchased in time period t and held for one year. The rate of inflation is the monthly annual rate of change in the HICP (Harmonized index of consumer prices) published by Eurostat. The HICP measure of inflation is lower but similar to the CPI (consumer Price Index) (Source: Central Quarterly Bulletin, December 2023 pp. 53-54).

Property is also an important asset for pension funds. Similar to bonds, property, especially commercial property has fallen considerably in value in Ireland and in other countries because of rising interest rates. In Ireland commercial property fell 14% in the year to September 2023 (Central Bank Financial Stability Review 2023, p. 19).

What about equities?

Apart from government bonds equites are an important asset for pension funds.

Equities are risky as shown in volatility in major indices over the last 25 years. Many indices are below their historic peak, for example the ISEQ index at year end 2023 was at 8779 compared with a historic peak of 10095 in May 2007. The Eurostox 50 was 4884 compared with 5712 at its peak in April 2000 (source:- https://tradingeconomics.com/ireland/stock-marke). The drop in real terms is much greater.

Index movements may not reflect returns because of dividends and the use of hedging instruments but are indicative.

Apart from long run movements in equities volatility in stock markets has been an important feature of all stock markets since the dot.com crash in 2000. Volatility adds to risk particularly around periods when accumulated funds are drawn down as pension income or cash.

Because of this risk many pension advisors suggest a switch to lower risk investment nearer to retirement. The Pensions Authority in Ireland recommends a ‘Life Styling’ approach to pension investments as follows; -

“Life-styling is an investment approach where contributions for each member are invested more heavily in higher risk growth investments, such as equities and property at younger ages and then gradually switched automatically to lower risk investments, such as bonds and cash as the member nears retirement” (Source:- https://www.pensionsauthority.ie/en/lifecycle/investment_risk_and_reward/default_option_and_lifestyling/).

This investment advice is in direct contrast to proposals by Colm Fagan (Irish Times 4th Jan 2023). He writes “The Government’s plan for pension auto-enrolment is flawed - there is a better way”

“An alternative approach would give members higher benefit expectations for two-thirds the cost and provide better inflation protection in retirement”.

Fagan states “higher returns would be achieved by remaining fully invested [in equities] at all times”. In addition, the proposal is that employees remain members of an AE scheme and only draw down a faction of their accumulated lump sum post-retirement.

An extended version of the Fagan proposals is available at :- (https://web.actuaries.ie/sites/default/files/2021-01/AE%20paper%20for%20SAI%20CFagan%206%20Jan%202021.pdf)

More controversially Fagan states that there is (p. 2) “.. ..too much emphasis on market values, which are largely irrelevant for the committed long-term saver”. Instead it is proposed that ’ transactions with the scheme, both as contributors and as claimants, take place not at market values but at smoothed values”.

Effectively rather than having individual accounts members of the scheme would be subject to the aggregate returns of the fund.

The Assumed Equity Risk premium

A key assumption of equity investment strategies) is that the equity risk premium is positive. The Fagan proposals assume it is 4% per annum.

Many studies of the equity risk premium are produced by financial institutions (Fagan cites Barclay Banks study of the annual equity gilt market for 2018).

While acknowledging (p. 18) that “no one can predict the equity risk premium, particularly over the next 70 years or longer”, Fagan states that “The only thing we can be sure of is that it must be positive in the very long-term”.

This raises the issue of choices between short run versus long run benefits. This choice is expressed in Keynes famous phrase “In the long run we are all dead”. It may also be the case that short run expenditures, for example on education are more valuable than long run expenditures for example on pensions.

Measuring the equity risk premium is technically challenging. In theory it refers to expected future returns. In practice it is defined as the difference between the yield on the lowest risk government bond and the yield on equity shares. The lowest yield government bond is assumed (in much research) to be the yield on US Treasury bills.

One problem is how can this extra return from investment in equities be explained. If markets reflect all information, returns from all asset classes, adjusted for risk should be the same.

Stock markets post the 2000 dot.com bubble have become more volatile. The Eurostox had a long term peak in 2007. Since there were six major falls and it is now below the 2007 peak.

This means an equity risk premium calculated using this index, would be heavily influenced by the time period chosen.

There may be Survivor bias. The composition of all indices varies through time. For example, the FTSE 100 index includes firms based on their market capitalisation. As market capitalisation changes so does the index and the calculated equity risk premium may be different from any given portfolio. Using a value weighted index based on a world portfolio.

Returns may be difficult to define. Stock market indices do not include dividends and their composition also changes through time;

Index construction is important, for example use of an arithmetic or geometric mean can lead to different results.

Other research indicates that over the very long term (> 100 years) returns are heavily influenced by whether a country has suffered some catastrophic event (war or invasion – Germany, regime change - Russia) (see:- file:///C:/Users/X1%20User/Downloads/SSRN-id1940165.pdf.) In particular some argue that equity risk premia for the U.S. are atypical (Jorion and Grotzman, Journal of Finance, June 1999, Table 1). They state (p. 978) :-

“.. .. the 4.3 percent real capital appreciation return on U.S. stocks is rather exceptional, as other markets have typically had a median return of only 0.8 percent”.

Returns for Sweden and Switzerland are also exceptional.

Conclusion

The introduction of Automatic Enrolment will lead to substantial changes in the Irish pension system.

Recent events in Government debt and other markets have drawn attention to the inherent risks of a funded pension scheme.

Investing in equities changes the nature of investment risk, but does not eliminate it and could increase risk.

The essential point of a pension system is to transfer future resources from those at work to those not at work. The key issues are:_

What Is the most efficient means of achieving this transfer?

What is lowest risk and What is equitable?

No pension system can be organised without cost and without risk.

Prof Jim Stewart

Dr Jim Stewart is Adjunct Associate Professor at Trinity College Dublin. His research interests include Corporate Finance and Taxation, Pension Funds and financial products, Financial Systems and Economic Development.

He is widely published and his titles include Mutuals and Alternative Banking: A Solution to the Financial and Economic Crisis in Ireland (2013), Choosing Your Future: How to Reform Ireland's Pension System (co-author, 2007) and For Richer, For Poorer: An Investigation of the Irish pension system (2005).

Share: