Cormac Staunton: In the immediate aftermath of the budget, there is much talk of whether the changes in income tax and USC were ‘progressive’ or not.

In order to be considered progressive, changes to the tax system should close the gap between those on higher and low incomes. As such, the cash benefit should be greater for people on lower incomes.

Changes to the tax system that give a greater percentage benefit to a person on lower incomes (even though the cash benefit is lower or the same) could be considered ‘less regressive’.

Using these definitions, changes to Income Tax and USC in Budget 2015 were not progressive, nor even "less regressive".

We modelled the changes in USC and income tax using our existing tax model, which is based on the rules for a single person paying PAYE. We looked at both cash and percentage change in net income: that is to say, how much did take-home pay change.

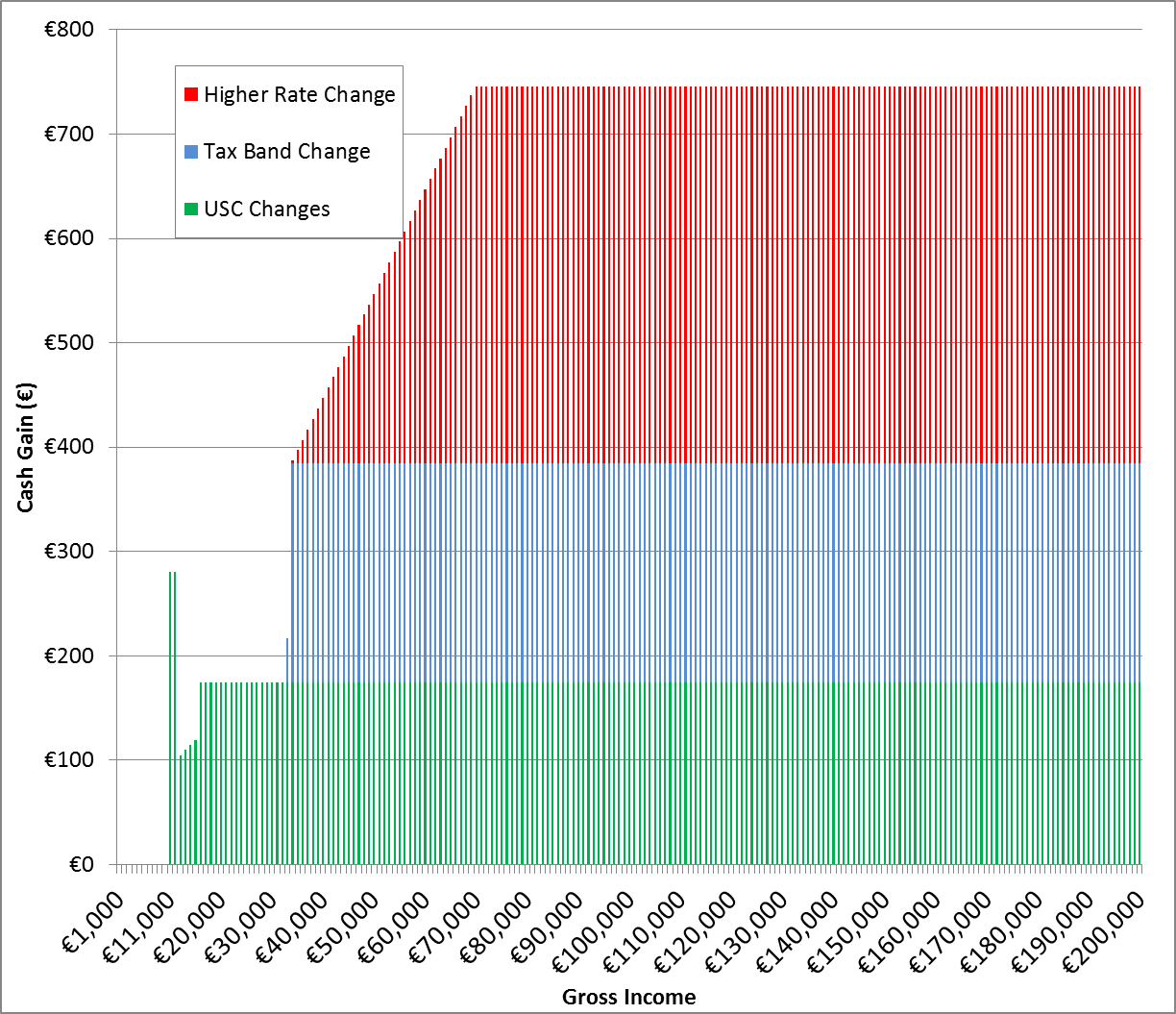

In cash terms it looks like this, when placed against gross income:

Those earning between €10,036 and €12,012 now pay no USC and see a benefit of approximately €240. This falls off immediately when USC kicks in, and between €12,012 and €17,500 (the minimum wage) the benefit of USC rate changes is around €110. From €17,500 upwards the gain from USC rate changes is €174.

After €32,800 the gains from income tax rate and band changes start to rise steadily, maxing out at €736 for those on €70,000, remaining at that level for all earners above €70,000.

Returning to our definition of progressivity, we should also look at what this means in percentage terms.

The curve shows that not everyone was affected proportionately. It can be explained as follows:

The first spike is caused by the removal of USC completely from people on €10,036-€12,012.

In the section from €13,000 - €32,000 the change in the USC rates and bands give a spike increase to people on the minimum wage as they are now out of the next level of USC. As we saw above, the absolute benefit from USC changes stays the same for all people above minimum wage and below €32,800 (as there was no change in standard rate of tax). Hence the benefit, as a percentage of take home pay, declines.

After €32,800 people are hit with a triple benefit. They have a lower rate of marginal tax (40%), a later entry point to the higher rate (by €1000), and they benefit from the changes made to USC on the earlier parts of their income.

This group is doing better in percentage terms than those below them (aside from the brief spike for people between €10,036 and €12,012) and the percentage benefit increases as incomes increase.

This is doubly regressive, in that firstly those on €34,000 see a significantly higher benefit than those on lower incomes, and secondly those on €70,000 have a greater percentage benefit than those on €34,000.

After €70,000 the same cash benefit remains, but because of the introduction of USC at 8%, the benefit no longer grows. Hence, as incomes rise, the percentage benefit declines, but long after the progressivity horse has bolted.

Whichever way you look at it, it is incorrect to describe the tax cuts introduced as “progressive”, given that the greatest benefit in cash terms is for the top 10% (above €70,000), and that the benefit in percentage terms increases steadily from those on minimum wages to those on €70,000.

Cormac Staunton is TASC's Policy Analyst. You can follow him on Twitter @Cormac_Staunton

Cormac Staunton @cormac_staunton

Cormac Stauton is currently a policy advisor on EU and international policy in the Central Bank of Ireland. Prior to this, he was a policy analyst in TASC, and co-authored the first economic inequality report, Cherishing All Equally.

Share: