Nat O'Connor: On an earlier post about indirect tax, I was asked to sketch out some principles about income tax.

Specifically, the questions were "how much income tax should everybody pay, and what proportion should that income tax be of the total tax intake? ... (a) at what point on the income scale should a person start paying tax, and at what rate and (b) at what point on the scale should the maximum rate kick in and at what rate ... So what do you propose in relation to entry level tax rates, and top tax rates?"

This is not meant to be a complete policy on income tax, as I'd need a lot more data (and time!) for that. But I am going to answer these questions in four parts. Firstly, I am going to set out some general principles for taxation. Secondly, I respond to the issue of people on high and low incomes not paying enough (or any) income tax. Thirdly, I am going to give some illustration of the effect of changing tax credits and bands. And then, finally, I am going to consider the question of how much tax someone should pay.

Part 1

Seven principles for taxation are that it should be stable, sustainable, adequate, progressive, efficient, transparent and responsive to economic, social and environmental externalities.

Stable – A stable tax system should be based on sources of revenue that do not fluctuate excessively as part of economic cycles. For example, this will require taxes on wealth, as well as income and consumption. Taxes on wealth (such as property tax) tend to be more stable during a recession. Property tax is common in many countries and is used to fund local government.

Sustainable – A sustainable tax is drawn from a source that will not become exhausted. Similarly, a sustainable tax system is not undermined by excessive tax expenditure.

Adequate –A country’s tax system must provide sufficient revenue to pay for the level of public services that people want, as well as other state liabilities, such as servicing the national debt.

Progressive – A progressive tax system is one where those who gain more from the economy (in terms of wealth and income) make a proportionately larger contribution. This should be the net effect across the whole tax system, not just income tax. Public services are one way of making the net benefit from the economy more progressive for people on lower incomes.

Efficient – Economically efficient tax is one which minimises economic distortion. The tax system should seek to encourage economic activity.

Transparent – All taxes, and to whom they apply, should be clear. In addition, all exemptions, tax relief, etc. should be transparent.

Responsive – The tax system also has role to play in influencing behaviour, by being responsive to market failure/externalities. Taxes can be used as policy tools to achieve economic, social and environmental goals. For example, carbon taxes discourage carbon-heavy activity such as burning of fossil fuels.

Note, sometimes these principles may be in tension. For example, responsiveness to externalities can conflict with progressivity, and hence something like carbon tax may need to be balanced with other measures, so that regressive effects do not occur which cost low income households disproportionately more of their income.

Part 2

In relation to income tax, the comment was made that "As things stand we have a very skewed tax take. The lower 50% of citizens pay no income tax, at the other end of the scale, neither do 4,000 individuals earning €100,000 +."

Sarah Carey claims that the facts about high earners not paying any tax are misunderstood, if not exaggerated. In particular, she refers to Section 23 of the Finance Act 2010, which increases the minimum rate of tax ('effective tax') from 20 per cent to 30 per cent that certain high earners must pay if they qualify for and use certain tax relief measures.

However, she misses the point that this only applies to "certain reliefs". Upon checking the relevant section (485C) in the latest Tax Consolidation Act guidance notes on Revenue's website, page 60, unrestricted reliefs (e.g. business expenses, other unnamed unrestricted reliefs) are always taken into account before restricted reliefs. Hence, there is some scope for someone to shrink their taxable income before the 30 per cent effective tax rate applies.

On the question of low paid people not paying income tax, the principle of progressivity requires the whole tax system to be progressive. So, there is not necessarily any problem with people on low incomes not paying income tax, if this compensates for the higher proportions of their incomes they pay in indirect taxation (like VAT), as I argue in the previous post. Also, as the worked examples below show, a single PAYE worker on €20,000 pays a small amount of income tax; so I don't think it can be true that 50 per cent of citizens pay no income tax, unless you are counting pensioners and people on social welfare. Certainly, most workers pay income tax; only those near the minimum wage do not.

However, the principle of adequacy requires that, if people want European levels of public services, then these have to be paid for. So, in order for the tax system to be adequate, everyone may need to pay more – although, in line with the principle of progressivity, those who benefit more from the economy should pay proportionately more.

Part 3

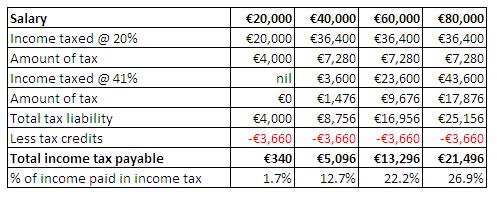

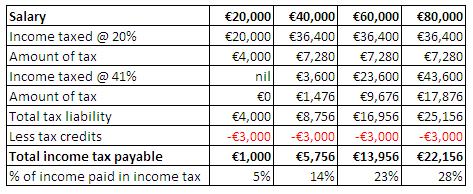

For reference, the current rates are 20 per cent on all income up to €36,400, and 41 per cent as the marginal rate. A single person gets €1,830 in personal tax credits. PAYE workers get an additional €1,830 (Citizens Information). For example, single PAYE workers on €20,000, €40,000, €60,000 and €80,000 would pay income tax as follows:

The Minister for Finance has announced Budget Day will be Tuesday 7 December. With all the talk of 'broadening the tax base', I guess that he will consider lowering tax credits and band thresholds, but not rates, in order to increase income tax on lower paid workers.

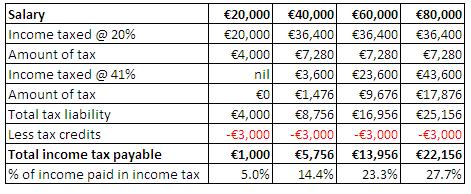

For example, if the single credit and PAYE credit were reduced to €1,500 each, our PAYE workers would now pay as follows:

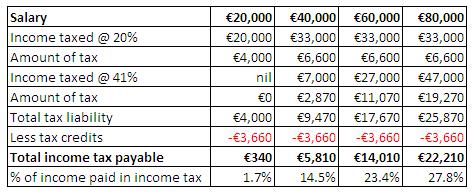

If the Minister instead chose to lower the marginal rate of 41 per cent to those earning over €33,000, a similar result would occur for those earning €40,000 or more, without increasingly the tax yield from those earning €20,000, as follows:

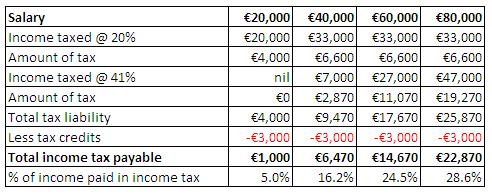

Obviously, this measure would generate less extra revenue overall. To maximise revenue, without raising rates, the Minister could combine both measures:

Now, all this is speculation, as I don't know what the Minister is going to propose. But I think it is worth pointing out the effects of changing credits and bands, as these kind of changes are often less obvious to people than rate changes, while they can have just as significant an effect.

Also, these examples give some facts and figures for illustration of the original question: how much income tax should people pay?

Part 4

I don't think increasing income tax is the best policy for Budget 2011, except maybe for those earning €100,000 plus. Instead, I'd prefer to see some kind of progressive system of property tax, as that would bring wealth into the equation as well as earned income. Since there are relatively few taxes on wealth in Ireland, that would be more progressive than simply increasing income tax.

In principle, in the medium term, as direct income tax (with higher marginal rates for higher earners) is more progressive than (flat rate) indirect tax, I'd prefer to see more tax on income and less VAT in the overall balance. Although, actually, I think any future increase on direct tax should be to address the low level of social insurance paid by employers and employees.

The last Budget unilaterly cut the amount of time people receive unemployment benefits for, as well as the amount paid, which shows how vulnerable the social insurance system is to political decisions. I'd prefer social insurance increases to income tax increases, alongside a more robust legal structure that gives people stronger guarantees about what level of benefit they receive when unemployed. In this context, I'd be quite happy to see much higher levels of unemployment benefit, which should be subject to income tax. But, as above, Budget 2011 is dealing with a jobs crisis, so it is not the time to increase social insurance, as to do so would increase labour costs and discourage job creation.

Income tax could be made more progressive. For example, Ireland is unusual in only having two bands (20 per cent and 41 per cent). There would be scope to have a third band, say 48 per cent, for incomes over €100,000. I would consider splitting up the existing bands too to have more bands with less difference between them. If the Government was to increase the standard rate of income tax, I think it would be important to increase personal credits, so that people on lower incomes are not made worse off.

Overall, I can't say what level income tax should be without access to a lot more data, namely costs for efficiently implementing West European standards of public services in Ireland, alongside data on the distribution of wealth and incomes. Such data would make it possible to calculate how much those services are going to cost (along with the banks and servicing the national debt). But we would be looking at moving towards Government tax revenue and expenditure at 45 per cent of GDP (which is still only average in Europe). The debt and banks may actually raise this much higher in the medium-term.

To conclude, I reiterate that everyone in Ireland pays tax – including indirect tax (VAT, excise, etc) – so I'll continue to dispute that only income tax counts when discussing 'broadening the taxbase'. As well as indirect taxes, new taxes on wealth (such as property tax) could have a significant role to play.

Ultimately, the taxation discussion should begin with what kind of public services people in Ireland really want. And when we can calculate the likely cost of these services, we can present people with a realistic tax model for how we can afford to pay for them.

It's at that point that democratic politics should provide people with real choice, depending on their preferences and how well or badly they'd do under each model. The conservative parties might continue to peddle low taxes, while they really mean returning public service spending to 35 per cent of GDP or less once the recession is over and the bank debt paid off. Progressive parties should be able to present a model of moving towards European norms at 45 per cent of GDP.

Dr Nat O'Connor @natpolicy

Dr Nat O’Connor is Assistant Professor of Social Policy at UCD, a fellow of the UCD Geary Institute for Public Policy and former Director of TASC. Nat also previously worked at Age Action, the Labour Party, Ulster University and the Homeless Agency. You can find him on LinkedIn (natoconnor) and TwitterX @natpolicy.

Share:

![Duggan, Vic]](/assets/img/2017/04/1491994913319631_sq.jpg)

{kind=link}