Michael Burke: In a recent discussion on this site, there are some important points raised about Ireland's external sector. This follows on from Governor Honohan's recent remarks in Asia, to the effect that foreign investors should note Ireland's exceptional export performance. The importance of foreign investors grows with every widening of the public sector deficit.

But the remarks and the subsequent debate have led to some confusion, not least because the remarks themselves are confusing. The external sector for most economies is the most ruthlessly competitive. Strong export performance indicates a high degree of competiveness. Yet many insist, the Governor among them, that Ireland is 'uncompetitive'. If by that is meant that the domestic sector should become more like the export sector; high skills, investment, wages, benefits (and even union densities), then there would be unanimity, or at least overwhelming popular support. Yet the opposite policy is being pursued.

Place in the Global Economy

It is widely known that this economy maintains a very substantial trade surplus. The surplus was ¤29.2bn in 2009, accounting for ¤1 in every 6 generated in GDP. The export total is greater than GNP, and is equivalent to 87% of GDP.

However, it is far less widely remarked that this economy has a substantial net balance of payments deficit on its current account, amounting to ¤4.9bn. This is the lowest current account deficit since 2004, and is largely a function of the collapse in import demand. It could be expected to widen once more in line with any recovery in domestic demand (graph here). The current account comprises in the main the merchandise trade balance, the balance on trade in services and net income from abroad. Both of these latter categories have been in substantial deficit over a prolonged period. The services' deficit was ¤8.4bn in 2009, while net income from abroad (which is overwhelmingly investment income) registered a deficit of €27.9bn, almost equivalent, by itself, to the trade surplus.

Before examining how this deficit is comprised, it is important to state its significance. All income is either consumed or saved. For each economy domestic investment and consumption must equal domestic incomes plus the savings of other countries, ie borrowing/lending from abroad. This current account deficit, despite huge trade surpluses, has led to increased net foreign borrowing. At the end of 2008, the net international investment position (the accumulated stock of assets/liabilities) was a deficit of €106bn, compared to a surplus as recently as 1998 (graph here). That stock of debt also requires debt-servicing payments, implying an increasing outflow of funds from this economy to service that debt.

So how is that debt accumulating?

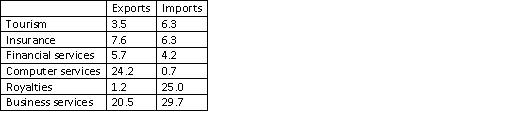

Net Deficits

Off-setting a huge trade surplus is a series of huge deficits elsewhere on the external accounts. But it is important to state that neither of these is provided by financial services, which is a minnow compared to other sectors, with imports of ¤4.2bn in 2009 and exports ¤5.7bn. Seven other (sub)sectors have greater degree of international openness. The main ones are set out in Table 1 below.

Table 1. Selected Service Sector Balances (€bn)

But there are two points to note- as before, financial services are a very small component of the overall trade in services and, secondly, the vast scale of the sums involved. To highlight the proportions, the value of business services' imports is equivalent to €15,740 for every person of working age in the State. Clearly, these services are not consumed in this State, they are either imports for re-export, or in the case of royalty payments, they are accounting method that reduces the taxable value of corporate profits arising from merchandise exports, or some combination of the two.

This accounting feature of the external accounts becomes obvious when the net investment account of the current account is examined. Here, the deficit was €27.9bn in 2009. The net investment account also has a number of components, but the deficit is almost wholly attributable to the deficit on income from foreign direct investment (FDI), which amounted to €27.1bn. This net outflow was almost equally comprised of the distribution of branch profits and the overseas reinvestment of earnings.

Foreign firms are booking profits here, but distributing them overseas. Because they are lsio doing that with sales, they create a net deficit on the curret account overwhelming the postive trade performance. They are also creating an increasign foreign indebtedness for the whole economy.

Who are the scammers?

The growth of FDI is one of the dramatic features of globalisation, allowing the increasing participation of all economies in world markets and the enormous efficiencies produced by investment to combine with the increasing (international) division of labour. For the host country, the benefits can be manifold, increasing employment, efficiency, skills' base, infrastructure and both export and taxation revenues.

However, by offering up this jurisdiction as a low-tax shelter, 'our international brand' as Messrs Cowen and Lenihan have it, and refusing to provide the necessary infrastructure investments, only the statistical benefit of fictitious exports has accrued, the rest is absent. In a recent Bloomberg investigation (highlighted here by Tom McDonnell), one US pharma company booked 70% of its sales through Ireland, even though less than 5% of its workforce is located here. And, contrary to the gombeen argument that 'well, at least we get 12.5% of that', the US company holds no special place in its heart for Ireland, further scams involving Bermuda, and employee-free subsidiaries in the Netherlands meant that it paid just 2.4% tax in Ireland.

These scams are overwhelmingly perpetrated by US companies. Ireland has a trade deficit in services with the US of some ¤17.4bn, whereas services trade with the Europe and the rest of the world is in surplus. US companies are not paragons of competitiveness, hence the US has the largest trade deficit in the world. Yet Ireland 'imported' €3.902bn from the US in market research services in 2008, and exported ¤1mn. Likewise there is a €3bn bilateral deficit in R&D, along with a ¤1bn deficit in management services and an enormous €7.5bn deficit in royalties, all with the US, while maintaining a balance or surplus with other geographical areas.

This scam has been facilitated by the actions of both governments, US and Irish, who are ware of these practices, yet have chosen to do nothing about them. However, of necessity recent US legislation is aimed at partially closing these loopholes. It might be an idea for the government here to move fast, before Uncle Sam's own deficit problems put Ireland in the Congressional cross-hairs.

A development-based approach to foreign investment would put a halt to these scams and raise the corporate tax rate, up to 20% (from lowest to second-lowest in the OECD). The huge increase in proceeds would be used to build up infrastructure, both material and educational, and allow the State to direct investment towards supplier industries for the foreign MNCs who actually produce here, including R&D, locking them into this location. In that way, the real success of openness to the world economy would be harnessed for sustained , high-quality growth, and the scammers could seek another jurisdiction to rip off.

Share: