Michael Burke: The Irish economy is in a Depression. Real GDP has fallen by 9.9% from its peak and real GNP by 13.8%. Even these terrifying data are flattered by the onset of deflation. Nominal GDP has fallen by 13.8% and nominal GNP by 18.5%.

The Government’s stated aim is to repair the public finances. Yet the crisis in government finances is a symptom of that economic slump, not its cause. The Government and its supporters argue that their actions have forestalled an even greater crisis- that revenues would have fallen further without tax increases and that expenditures would have climbed even higher without spending cuts. The argument for fiscal austerity stands or falls on this proposition.

This argument has been forcefully deployed. But it is false.

This can be shown by comparing the fiscal measures with the outturn in both government finances and the economy. Table 1. below sets out measures taken by the government in the name of restoring government finances and reassuring the financial markets. The December 2009 Budget measures, which will impact in 2010 and beyond, are not included. Those amounted to another €4bn in expenditure cuts.

Table 1. Budget Measures, 2008-2009

The total tax increase amounted to €5.944bn and the total cuts in expenditure amounted to €4.614bn, for a total of €10.558bn, equivalent then to 6.44% of GDP. It is argued that these measures prevented a further deterioration in government finances.

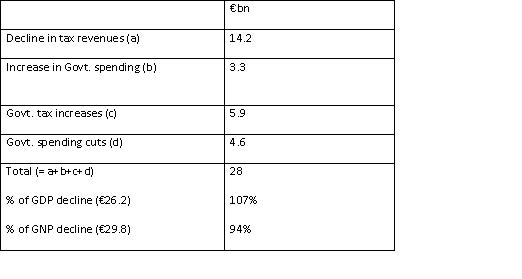

But this assertion has no merit. If it were true, then without the fiscal measures taxes would now be €5.944bn lower than currently and spending €4.614bn higher. Table 2. below sets out the actual change in both tax revenues and votes spending and adds these to Budgetary contraction measures, both spending and taxation, ie takes the government assertion at face value.

Note: all in nominal terms, for consistency with both the reality and accounting of government finances.

Table 2. Wishful Thinking on Slash&Burn- The Government Case for Cuts

Source: calculated from DoF, CSO data

We therefore arrive at the ludicrous situation where the Government and its supporters argue that they have saved Government finances from a far worse fate- one in which Government activity accounts for 107% of GDP. Even if the supposed effectiveness of fiscal austerity fell by 18%, it would still leave the State finances accounting for 100% of the change in GDP during the recession. Or if we apply the government’s preferred measure of GNP, the State finances are still equivalent to 94% of the change in GNP. This is not a serious proposition. It is a level of State dominance of the economy not reached even in the Democratic People’s Republic of Korea.

Instead, in national accounts government expenditure is a component of GDP and a part of investment (Gross Fixed Capital Formation). Cutting either depresses economic activity both directly and indirectly, as other sectors adjust to the lower level of final demand.

The alternative view, that government spending cuts can ‘crowd in’ private sector expenditure to replace it, has demonstrably failed to materialise. Since fiscal tightening began in late 2008 every component of GDP has declined, household consumption, government spending, exports and inventories have declined by. Declining investment remains the driving force behind the recession, with gross fixed capital formation falling by a further €10.4bn over that period. All sectors of private activity have fallen at much faster rate than the decline in public spending. They have not been ‘crowded in’.

Government finances are in crisis because of the collapse in tax revenues, based on the slump in private sector activity. Only the restoration of growth will restore those taxes, along with a balanced tax regime. Current policy is not working.

Share: