Michael Taft: This follows on from Nat O’Connor’s post on taxation and concerns an issue raised by Seamus Coffey in a considered comment; namely, how progressive is Irish taxation.

Reliance on Revenue Commissioners’ tables can only take us so far. There is much that is not included in this data. For instance, this only assesses income for the purposes of income tax. It doesn’t include capital income such capital gains, inheritances, gifts, etc. Even for the purposes of income tax, it doesn’t include all income. Revenue lists some of the income, profits or gains it doesn’t include (e.g. stallion fees, patent royalties, forestry profits, artists’ income, etc. - a list is attached to the Revenue tables). The Commission on Taxation also lists a number of exemptions which may not be included in the Revenue income tables.

Further, the Revenue tables don’t show social insurance payments, which are reduced for high income earners owing to the contribution ceiling (never mind that PRSI is not levied on capital income). And, of course, the tables don’t show the payment of indirect taxation which is regressive.

Using the Revenue tax tables to test the progressivity of the tax system is fraught with problems. Unfortunately, there is no single data source for a comprehensive view of income and taxation. However, the EU Survey of Income and Living Conditions can give us some pointers – as it includes more income and more tax than the Revenue tables. Of course, it is a survey – voluntary and subjective. Still, it is accepted as a reliable data source throughout the EU.

Using the 2008 equivalised income figures we find that the top 10 percent earn 31.7 percent of all direct income (income from work) in the state and pay 38.7 percent of all income tax and social insurance. While progressive, it is not overly so (for those in the middle 6th decile, most of whom earn less than average income – they earn 9.1 percent of all income and pay 7.9 percent of all tax/PRSI).

It should be noted that SILC includes employers’ PRSI in calculating both income and tax for individuals. This takes account not only of the ‘social wage’ but of real benefits such as employers’ contributions to pension, heath insurance, etc. benefits.

Effective Taxation

As to effective tax we find that the top 10 percent face a tax/PRSI liability of 29.7 percent. This contrasts to a national average tax liability of 24.4 percent. Again, this is at the softer end of progressivity.

We should note that SILC doesn’t take into account irregular income, of which inheritances and gifts would be a major category. Unfortunately, we don’t have a deciles breakdown of this income (if there is one, I would appreciate a source), but it is reasonable to assume that the larger proportion goes to high income groups. In this regard, a ‘child’ receiving €750,000 through an inheritance would face an effective tax liability of only 11 percent.

However, the main omission from the above calculations is VAT and other indirect taxes. That SILC omits this is understandable – respondents in a survey are not in a position to identify the amount of VAT they pay.

The ESRI and Combat Poverty Agency assessed the distributional impact of VAT and excise taxes and found that the top decile paid less than 10 percent of their income on indirect taxes while the poorest 10 percent paid nearly 21 percent. This shouldn’t be too surprising as indirect taxation is generally regressive.

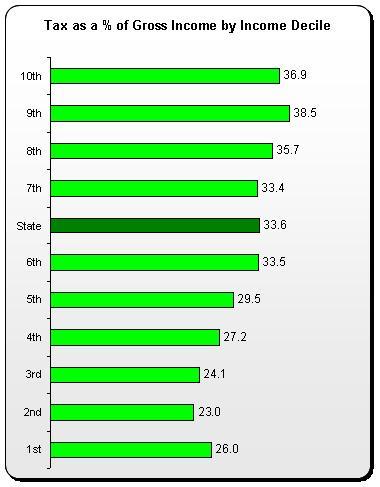

The following applies the findings of the ESRI/CPA on the SILC data using gross income (including social transfers). This is not wholly satisfactory. First, we are dealing with different data sources. Second, the indirect tax data was published in 2005 based on the 2000 Household Budget Survey – so it is a bit dated. The following, therefore, should not be taken as conclusive but rather serve as an indicator.

As can be seen from the chart, when indirect taxation is included, the tax liability of the highest income group – 37 percent – is not much more than the national average – 34 percent. Given that the lowest income decile pay 26 percent, the level of progressivity is highly limited.

To repeat, this is just an exercise. However, we shouldn’t be too surprised at the lack of progressivity in the Irish taxation system. Eurostat finds that Ireland relies more on indirect taxation than any other EU-15 country. Whereas indirect taxation makes up, on average, less than 35 percent of all tax revenue in other EU-15 countries; in Ireland, it makes up 43 percent. This heavy reliance on regressive taxes is likely to undermine a progressive tax base.

In conclusion, while we still wait for a comprehensive survey of taxation and income, there is evidence to suggest that progressivity in the Irish tax system is limited. If, as Nat suggests, that we will need to substantially increase taxation, it is imperative that we not only define strategies that are the least deflationary and the most equitable; we need to get an accurate picture of the equity, or lack of, in the current system.

Michael Taft @notesonthefront

Michael Taft is an economic analyst and trade unionist. He is author of the Notes of the Front blog and a member of the TASC Economists’ Network.

Share: