Nat O'Connor: We are coming up to the first anniversary of Lifetime Community Rating (LCR) in private health insurance and it is timely to consider how this policy reinforces Ireland’s multi-tier health system and entrenches income inequality.

The previous government introduced LCR in May 2015, affecting everyone aged 34 or older. For every year a person does not hold health insurance, he or she must pay an additional 2 per cent per annum on the cost of an annual health insurance premium.

For example, someone who first takes out health insurance aged 39, five years beyond the age threshold, will pay a 10 per cent additional cost for life; so a €2,000/year premium* will cost that person €2,200/year instead. This adds up, and with the added unknown of health insurance price inflation, the crude percentage increase caused by LCR could have an even greater effect.

(* An average premium of €1,925 in 2015 was cited by a survey carried out for the Health Insurance Authority/HIA, although most people goaded into taking up insurance by LCR appear to be paying around €1,000 for the cheapest policies; schemes that come with so few benefits that serious questions could be asked about them).

But wait, wasn't LCR motivated by equality, or at least solidarity between the generations? LCR pushes younger people to sign up to insurance, which keeps the system funded (and the majority of insurance beneficiaries are older people or people with long-term illnesses). In theory yes, but if someone has a poor start in life or has many demands on their income (from children, disability, elderly relatives, siblings, or whatever) he or she may simply not be able to afford to buy health insurance until later in life – and he or she will be punished by the LCR system for this.

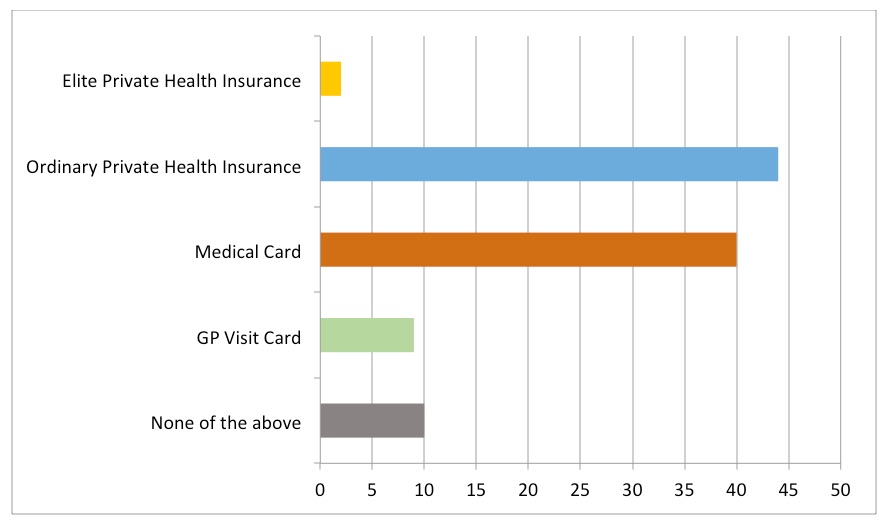

Ireland’s health service is not, as is sometimes said, two-tier. This is usually meant to refer to some kind of vague public-private divide. But upon examination such a simple divide does not exist. Ireland’s system has at least five distinct tiers, with nuances within them as well as between them. The tiers need to be understood from the point of view of households trying to access health care services.

At the top of the system are a small elite group: those with sufficiently high incomes that they can afford gold-standard private health insurance, which allows them to access the best of what health care services in Ireland can provide. Not only does this include private rooms in public hospitals and private consultations given in public facilities, but insurance cover for the full range of exclusive private medical facilities too.

There is a large group in the second tier who might be described as those having ‘ordinary’ private health insurance. They pay an ‘excess’ on medical bills before they can call upon their insurance to pay the rest, and their policies do not cover all of the high-end private medical facilities. There are, of course, hundreds of different insurance policies available – so there are nuances within this group in terms of what individuals can or cannot access with their insurance policies. Along with private and ‘semi-private’ rooms in public hospitals, their main benefits is accessing outpatient services and tests (diagnostic services).

According to the same major survey by the HIA, nearly 46% of the population now have some form of private health insurance. This 46% of the population includes the small top tier too, but the large majority will be in the second tier of ‘ordinary’ private health insurance. (A guesstimate is that 1 in 20 holders of private health insurance, c. 2.3% of the population, have one of the top tier policies; but this could be wrong).

It is striking that the research by the Vincentian Partnership for Social Justice on a minimum essential standard of living (MESL) found that although their focus groups could agree on a very frugal standard of living across many categories, having a basic level of private health insurance was felt to be a basic requirement in our society.

The HIA survey found “a strong belief among a substantial minority of PHI holders (27%) that public services are of an inadequate standard, and that there is a lack of access to such services (18%).” Furthermore, “there is a broad consensus across the population as a whole that having PHI [private health insurance] means you can ‘skip queues’ (58% believe this to be the case, albeit down seven points since 2013). In addition, a majority (56%) agree that ‘having PHI means always getting a better level of healthcare service’, and that ‘PHI is a necessity, not a luxury’ (56%).”

It seems reasonable to suggest that holding private health insurance is a common expectation in Irish society. As such, if LCR does exclude the lowest paid workers from accessing health insurance this should be seen as problematic (even for those who might prefer to scrap the insurance model in favour of establishing a tax-funded Irish NHS or some other model of health care funding).

The third tier in the Irish health care system comprises those with the lowest incomes in society (or certain medical conditions), as well as the over-70s, who are covered by a Medical Card. According to the HSE, as of October 2015, 1.8 million people have a Medical Card (c. 40% of the population). This entitles them to free-of-charge GP services, subsidised medicines, hospital services, dental and optical services, etc.

The fourth tier in Ireland’s health care system are those on quite low incomes who qualify for a GP Visit card, but not a full Medical Card. This gives relatively few entitlements, but means they do not have to pay the typical fee of €50 to see a GP. According to the HSE, 410,000 people (c. 9% of the population) receive a GP card. That number will now include all children under the age of 6. (Budget 2016 included provision to extend to this to all children under 12, subject to negotiations with the Irish Medical Organisation; see CIS).

It should be noted that some people with a Medical Card or GP Visit Card also purchase private health insurance. For example, someone with a particular medical condition or disability might do so in order to access certain treatments or simply to gain a faster response to their needs. Moreover, some of the c.330,000 over the age of 70 with a Medical Card may also have sufficient incomes to afford private health insurance too.

As such, we cannot simply add the numbers with private health insurance (46%), Medical Cards (40%) and GP Visit Cards (9%) to deduce that the remaining 5% have none of the above. One survey suggests that 25% of people have neither a Medical Card nor private health insurance (Pfizer Health Index 2015, cited in the Irish Independent). The Pfizer survey has quite different findings from the HSE and HIA for the numbers with Medical Cards (44%) and private health insurance (36%), which suggests caution is needed before accepting the 25% figure outright. It is also probable that those with GP Visit Cards are among this cohort.

Nonetheless, conservatively, it might be safe to assume that at least 10% of people have not got a GP Visit Card, a Medical Card or private health insurance. And the real figure could be higher.

Hence the bottom, fifth tier comprises those without private health insurance, Medical Cards or GP Visit Cards. They are likely to have higher incomes than those who receive the state-provided Cards. They are more likely to have incomes from employment. Yet they are definitely the worst off in Ireland’s health care funding system. Nonetheless, they do have access to Ireland's public health services (more details below).

Having established this framework, consider what LCR does.

It seems reasonable to assert that many of those in the 10%+ cohort do not purchase private health insurance because they cannot afford it. Similarly, for the 9% with only a GP Visit Card.

Over half (53%) of those dropping private health insurance in the HIA survey cited their inability to afford it or that it was too expensive. A further 11% said it no longer represented value for money and 6% cited the loss of their job. And 12% mention that they dropped it because they had a Medical Card. Only a small cohort (5%) said that they were healthy/‘don’t need it’ as a reason to drop private insurance. Conversely, in the same HIA survey, 62% would take out private health insurance if they ‘had more money’ or if premiums were cheaper.

Inadequate income is clearly the main barrier for a lot of people when it comes to taking out private health insurance. This is consistent with the fact that there is a substantial group of people who work for far less than a Living Wage in Ireland - a standard of living that, among other things, would enable someone to afford basic health insurance.

Some people in the bottom two tiers will never earn enough to afford private health insurance, but neither will they be eligible for a Medical Card – except upon retirement when their incomes are likely to drop below the eligibility threshold.

However - and this is the negative, direct effect of LCR - if anyone from low to middle income groups do work their way to a higher income after the age of 34, they will pay more for private health insurance than those who have already been more fortunate in life.

Similarly, if someone moves from reliance on social welfare to a higher income from employment, he or she will also be penalised by the LCR rule; e.g. this will include full-time carers returning to work when an elderly parent they cared for passes away.

Hence, not only is there a new welfare trap created by LCR, but there is also a penalty placed on workers employed in low-wage sectors. In particular, part-time workers (who are overwhelmingly women who also do unpaid work in the home) are badly affected by LCR.

LCR is a manifestly unjust policy. Whatever about its goal of pushing young people to buy insurance in order to prop up the system, any increase in intergenerational solidarity comes at the price of reinforcing and deepening income inequality. LCR creates yet another barrier to working people who seek to attain a minimum, decent standard of living for their families.

Some would argue that the public health service is good enough and health insurance is unnecessary or even a con. It should be remembered that the HSE does provide an extensive range of services, which are highly subsidised (e.g. hospital stays are capped at €75/night and €750/year maximum, far less than the actual cost). It is probable the public health service provides the best available service for many things, including A&E, maternity services and acute illness (which is not to say that it can’t improve, but that private medicine is not offering anything better). But where health insurance appears to come in most useful is for the two major killers: cancer and cardio-vascular (heart-lung) disease. Whenever anyone has to wait to get a check done in order to get a diagnosis, and must wait again to see a consultant, health insurance may get things done much quicker – which can make all the difference. Slow access to orthopaedic services in the public system (e.g. for hip and back issues) is another area where those without private insurance can suffer unnecessary disability for years while they wait. Put simply, Ireland has a system where poor people are forced to wait longer for the same tests, and are therefore more likely to suffer or even to die due to the advancement of their illness before they finally receive treatment.

Forcing everyone to buy private health insurance - especially very cheap policies that do not offer many benefits - is not the most efficient or socially just way to address the deficiencies in the health system. A coherent funding mechanism is needed, but Ireland's hybrid system offers a bad combination with inherent contradictions and inequalities.

There is a lack of clarity about to what extent those with insurance are allowed to skip people without insurance in the same queues. But it does seem to be the case that those with insurance can step out of the public queue and ‘go private’ in order to get tests done quicker elsewhere, before bringing these results back with them into the public system. Certainly, the majority of people (58%) surveyed by the HIA believe that private health insurance allows people to ‘skip queues’. To the extent that this is possible, it is morally twisted. And Lifetime Community Rating only makes the system worse.

Nat O’Connor is a lecturer and researcher at Ulster University and a member of TASC’s economists’ network.

Dr Nat O'Connor @natpolicy

Dr Nat O’Connor is Assistant Professor of Social Policy at UCD, a fellow of the UCD Geary Institute for Public Policy and former Director of TASC. Nat also previously worked at Age Action, the Labour Party, Ulster University and the Homeless Agency. You can find him on LinkedIn (natoconnor) and TwitterX @natpolicy.

Share:

![Duggan, Vic]](/assets/img/2017/04/1491994913319631_sq.jpg)