Cormac Staunton: The National Economic Dialogue concludes today. The Department of Finance have published guiding documents for each of the breakout sessions. They state that they should “not be seen as prescriptive but rather seeks to set out the current factual situation and to suggest some of the key questions which participants may wish to consider”.

Here are a few comments on the ‘factual situation’ as presented in document for the Economic Growth and Equity in Tax Policy group.

Tax Level

Measured as a proportion of Gross Domestic Product (GDP), Ireland has a relatively low tax burden by European standards according to the latest data. In 2012 total taxes were 28.7% of GDP compared to the EU-28 average of 36.3%. However, given the exceptional gap between GDP and Gross National Product (GNP) in Ireland, the Irish Fiscal Advisory Council (IFAC) have argued that a more appropriate measure of fiscal capacity is a hybrid measure taking GNP plus 40 per cent of the gap between GDP and GNP. On this basis, the tax take share rises to 32.4%Even on this basis Ireland is still below the EU average tax base.

Social Security

If social security contributions (SSC) are excluded from the comparison (given the stronger insurance character of these systems in other EU countries compared with Ireland), the tax take at 24.3% of GDP is marginally below the EU-28 average of 25.2%. As a percentage of the IFAC measure this rises above the EU average to 27.5%.There is no reason to exclude SSC from this analysis. However, doing so only goes to highlight the low level of social security in Ireland. In fact Ireland has the second lowest social security contributions in the EU. This helps to explain our low effective tax rates in comparison with other OECD countries:

Effect of Tax on Inequality

In Ireland, the reduction in the Gini coefficient (a measure of income inequality) between market incomes (i.e., before taxes and transfers) and disposable incomes is greater than in any other OECD country reflecting the progressive nature of the income tax system and the effect of transfers.It is important to note that transfers play a far greater role than taxes:

- Gini before taxes and transfers is 56.8

- Gini after taxes, before transfers 53.8

- Gini after taxes and transfers: 31.2

Progressive Tax and Employment

This progressivity entails high marginal tax rates which affects labour force participation and individual decisions on how much to work.To be clear, high taxes can have both positive and negative effects on labour force participation and individual decisions on how much to work. The 'substitution effect' says that if taxes are high an individual will work less. But the 'income effect' means that if taxes are high an individual will work more.

Tax cuts versus expenditure

In light of the anticipated fiscal space of €1.2–€1.5 billion to be split 50:50 between tax reductions and expenditure increases, what would be the best use of the circa €600 - €750 million available for use on the tax side?The 50:50 split is a government decision. Discussions should also be about the appropriateness of the 50:50 split itself. It could be weighted 2:1 in favour of expenditure increase, or indeed could all be put to public investment.

A recent Behaviour and Attitudes Opinion Poll showed that nearly 7 out of 10 Irish people would prioritise investing in public services over income tax cuts.

Tax 'Burden'?

How can reductions in the tax burden be managed without excessively narrowing the tax base?Why are taxes constantly referred to by the pejorative term ‘burden’? Given that we have a below average tax take, why is there an assumption that we always need to reduce taxes?

A barrier to growth?

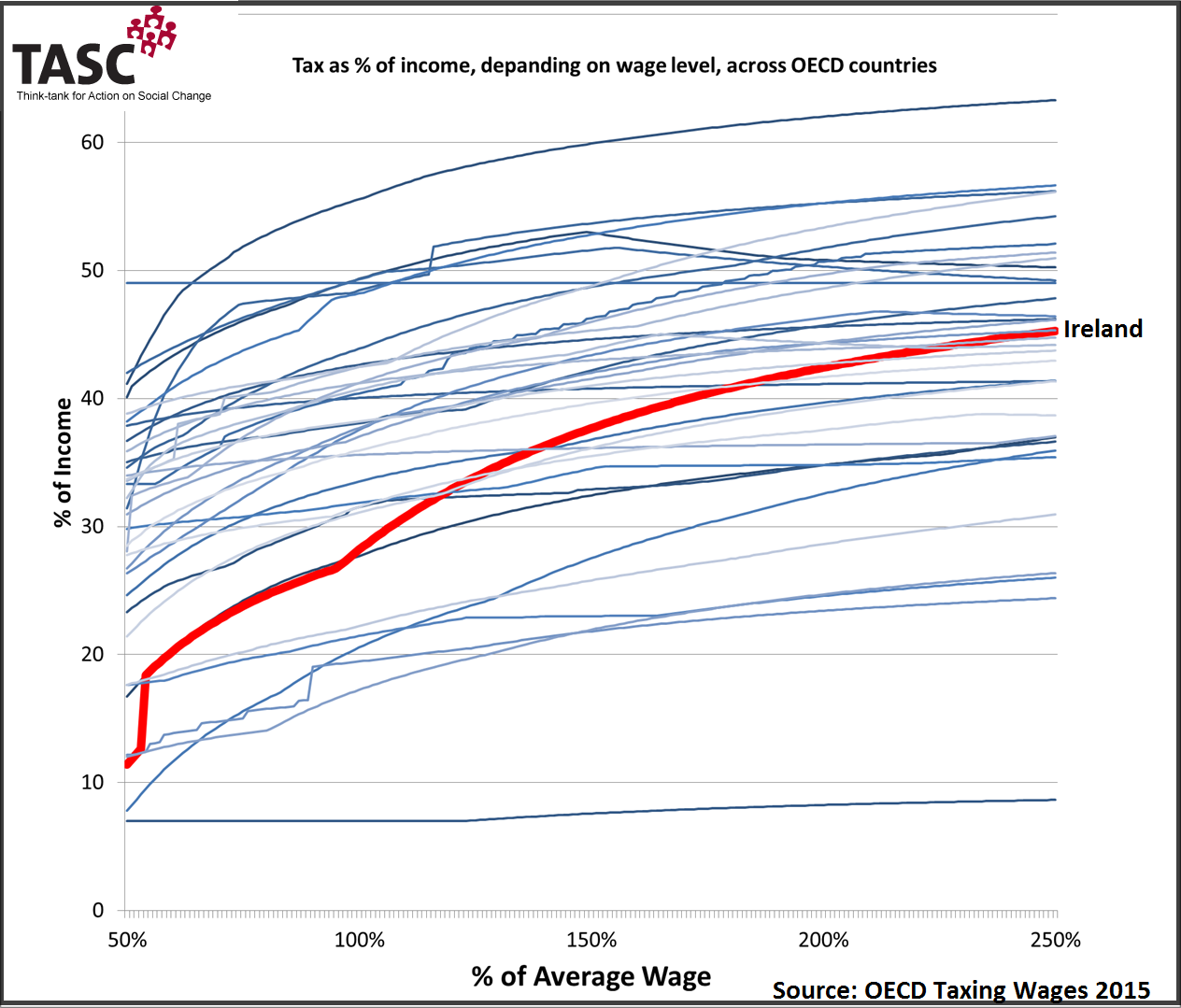

In a highly competitive international market for highly skilled mobile individuals, is the highly progressive nature of the Irish income tax system a barrier to sustainable growth?Effective tax rates, even at the top end, are around average for OECD and far below some competitor countries (see chart above). Evidence to support the fact that the 'progressive nature' of the tax system might be a ‘barrier’ to growth should be based on robust evidence.

Is progressivity equitable?

Are the high levels of progressivity of the Irish income tax system truly equitable? Is it right that the top 1% of income earners pay 20% of the total income tax and USC collected while almost 30% are exempt entirely?This also shows the high degree of inequality in incomes. Ireland has the highest level of pre-tax, pre-transfer inequality in the OECD.

Cormac Staunton @cormac_staunton

Cormac Stauton is currently a policy advisor on EU and international policy in the Central Bank of Ireland. Prior to this, he was a policy analyst in TASC, and co-authored the first economic inequality report, Cherishing All Equally.

Share: