Cormac Staunton: There has been a lot of talk recently about cutting income taxes now that the Irish economy is beginning to show signs of recovery. Everyone loves a tax cut, but it’s worth looking at what is being proposed, and who is really going to benefit.

From the outset, it’s important to point out that what is being referred to as a tax ‘cut’ is in reality a widening of the tax bands so that the higher rate (41%) kicks in a bit later than it currently does (€32,800). The effect of this type of ‘cut’ won’t be the same for everyone.

The first and most important thing to note is that if a person doesn’t earn more than €32,800 per year, then this change will have no impact on their take home pay. Given that more than half of Irish workers do not earn that much, then that is a significant amount of people who won’t see any benefit from the tax cut.

It is also important to point out that 41% is a ‘marginal’ rate, which means everyone, no matter how much they earn, pays 20% on their income up to €32,800, and then 41% on anything earned above that.

To show the impact of widening the tax bands, we therefore need to see how it would change a person’s ‘effective’ tax rate, the amount of tax they actually pay.

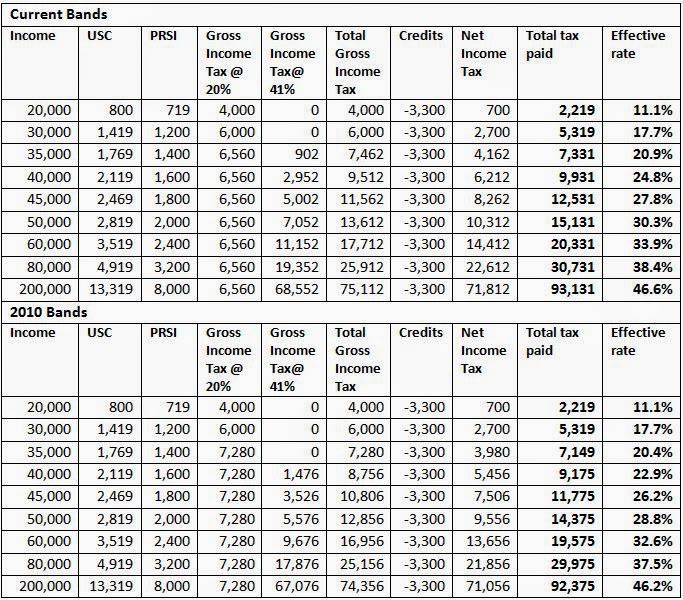

We can show effective rates (including USC and PRSI) using tools such as the Deloitte Tax Calculator. We can then compare two different scenarios (for a single person); the current system and a hypothetical system where the tax band has been widened. As an example, we can show what would happen if threshold was raised from €32,800, to €36,400 (which is where the cut off was in 2010) to see who benefits from a widening of the bands.

The results are:

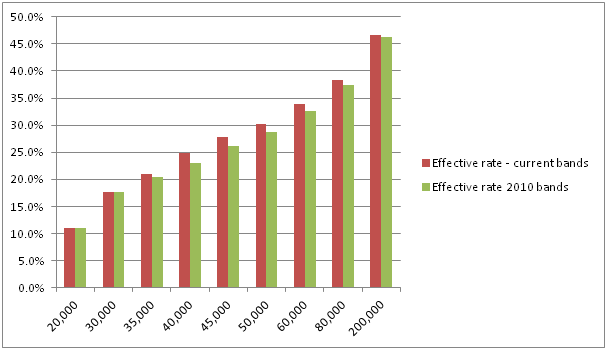

In chart form, the change in effective tax rates look like this:

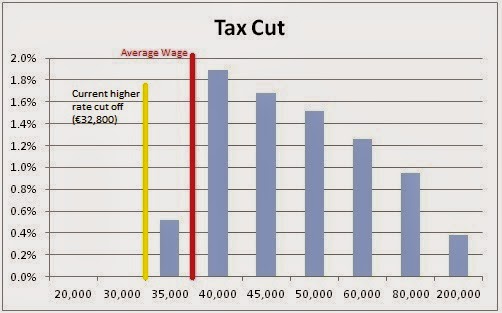

It is often presented that the greatest benefit of this type of cut is for those earning just above the current cut-off (between €32,800 and €36,400), who will now pay no taxes at the higher rate.

However, because it is a marginal rate, this is not the case. The real benefit goes to those who pay more of their income at a higher rate. From the figures above it is clear that those who benefit most from this tax cut (in percentage terms) are those earning €40,000 per year, who would get a 1.9% cut. These are people on above average incomes.

Widening the band would also bring significant benefits (in real terms) for those on much higher incomes; 1.5% for someone on €50,000, 0.9% for someone on €80,000 (and note; this does not take into account other forms of tax breaks available to higher earners).

At the same time, those earning around average wages (c. €35,738) see a much smaller benefit (0.5%). And crucially, these figures confirm what we already knew: that this type of change would be of no benefit to around half of all workers in Ireland who earn less than €32,800.

Given that 20% of workers in Ireland are officially on low pay, one of the highest levels in western Europe, and that manual workers’ wages have fallen since 2010, while managers and professionals have increased their wages in that time, it is likely that that widening the tax bands would widen the already high levels of income inequality in Ireland today.

Cormac Staunton is TASC's Policy Analyst. You can follow him on Twitter @Cormac_Staunton

Cormac Staunton @cormac_staunton

Cormac Stauton is currently a policy advisor on EU and international policy in the Central Bank of Ireland. Prior to this, he was a policy analyst in TASC, and co-authored the first economic inequality report, Cherishing All Equally.

Share: