Donal Palcic and Eoin Reeves: Yesterday the Minister for Transport signalled the possibility of selling the remaining 25 per cent stake in Aer Lingus (as recommended by the report of the Review Group on State Assets and Liabilities published last April). News of other planned sales, such as the sale of a partial stake in the ESB, is expected over the coming days. So does the sale of the remaining government held shares in Aer Lingus make sense? This can be assessed in terms of the government’s objectives. First, this is about raising exchequer revenues, so how much can the government expect to realise? With shares trading at 67.5 cent as of this morning (compared to the IPO price of 220 cent) a 25 per cent stake is likely to be worth in the region of €90m (leaving a lot more to be sold if the €2bn target in the programme for government is to be reached). Net revenues will of course be reduced when professional expenses and discounts are taken into account.

Are there any other advantages to be accrued from the mooted sale? The common argument in support of selling state owned enterprises (SOEs) is that performance will improve under private ownership. But Aer Lingus operates as a privately owned enterprise and is not subject to obvious political interference (a problem traditionally faced by some SOEs). So selling the remaining 25 per cent will not have any impact in terms of improving enterprise performance.

What are the likely downsides to the possible sale? The obvious one is that the 25 per cent stake constitutes an important degree of state influence over the island economy’s airline. We have discussed the importance of the state retaining control over strategically important industries before here and here. But suffice to say that Eircom provides an example of one of the biggest privatisation failures worldwide and this could have been avoided if the state had not relinquished complete control when it privatised the company. The lessons in relation to Aer Lingus are obvious.

One of the big strategic issues in relation to Aer Lingus concerns the Heathrow slots. The Minister for Transport stated that the strategic reasons for retaining a stake in the airline no longer exist and that the issue of Heathrow landing slots was not as important as it was since people are now using connections other than Heathrow. Aer Lingus has 23 landing slots in Heathrow. Currently 13 slots are being used on the Dublin route [BMI also operates on this route and has 4 landing slots], 4 on the Cork route, 3 on the Shannon route and 3 on the Belfast route.

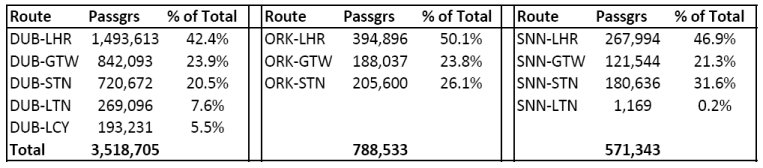

Data from the UK’s Civil Aviation Authority shows that, in 2010, over 9.5 million passengers travelled from the Republic of Ireland to the UK, with just over 51 per cent of all passengers travelling to London. A quick glance at the traffic on the Dublin, Cork and Shannon to Heathrow routes for 2010 (see table above) illustrates the importance of the Heathrow link, with slightly over 44 per cent of passengers to London going through Heathrow. In general, the vast majority of passengers from Ireland to Heathrow are carried by Aer lingus (they are the sole operator from Cork and Shannon; while on the Dublin Heathrow route they operate significantly more flights than BMI).

While the number of passengers travelling to airports in London other than Heathrow has increased considerably over the years, based on the above figures for 2010, it is hard to see how the Minister can claim that the “strategic” argument for retaining a stake in Aer Lingus no longer applies. For an island nation like Ireland, which is heavily dependent on international connectivity, the Dublin/Cork/Shannon to Heathrow routes are of considerable strategic importance. Although the sale of the government’s 25 per cent stake does not mean that flights on these routes will stop overnight, it does leave the government powerless to prevent an undesirable change in ownership in the future (think Eircom).

Given the relatively small amount of cash that is likely to be raised, one must question whether this mooted proposal makes sense. Our scepticism appears to be shared by the company itself, which reportedly is not in favour of a quick sale. Moreover, Joe Gill of Bloxham sounded a sceptical note when interviewed by Matt Cooper on Today FM yesterday. Mr. Gill raised the issue of the Heathrow slots and also highlighted the difficulties posed by the company’s pension deficit (in the region of €400m). He also suggested that a special dividend by cash-rich Aer Lingus (it has cash balances of approximately €350 million) offers an easier way for the government to raise much needed cash from the company. Notwithstanding the issues that arise in forcing a special dividend one wonders if this route makes more sense than relinquishing full control over the airline.

Share: