Michael Burke: The Irish Times reports that the new Taoiseach refused to countenance any upward adjustment of the corporate tax rate in exchange for a lowering of the punitive tax rate applied to EU bailout funds.

The EU offer highlights the scandalous nature of their impositions, which is charging Irish taxpayers 3% more than its own cost of funds – to bail out EU banks. The offer was to reduce that premium by just 1%, which would provide a saving of €450mn per annum in lower interest payments. As already highlighted here, the FT’s Martin Wolf has argued: “For a sovereign to destroy its own credit, to save creditors of its banks, is plainly wrong. It does not make it better, but worse, that it is doing so largely to protect financial systems in other countries.”

There is a loss of sovereignty, even a conscious effort at national humiliation arising from this destruction. It can be regained, in the first instance by the State refusing to absorb bank debt.

But that does not mean that the insistence on maintaining ultra-low Irish corporate tax rates fulfils the requirements of this economy or its fiscal position. The 12.5% tax rate is the lowest in OECD. The next lowest is Iceland’s 15% - which ought to be a warning sign by itself. The highest corporate tax rates in the OECD are 39% in the US and Japan. Other ‘small open economies’ such as Denmark, Finland, Greece and Portugal all have much higher corporate tax rates (although the large waivers and exemptions, such as to the Greek shipping industry and its millionaires, are significant contributors to their fiscal crises).

Relocation

In all the commentary about Dell’s decision to relocate to Poland, there was little discussion of the fact that it has a higher tax rate, 19%. What is also has are large transfers from the EU, which are being used for investment purposes, especially in infrastructure, transport and communications.

There is no doubt that many producers argue vociferously for the maintenance of 12.5%. IBEC and the US Chambers of Commerce have been particularly vocal on this and threatened relocation if there is any adjustment. However, if all capital were absolutely mobile and primarily determined by tax rates, then ultra-low tax rates would have already attracted all Foreign Direct Investment (FDI) in the OECD to Ireland. That is plainly not the case.

Most of IBEC’s members cannot relocate anywhere- they service demand in this economy. Likewise for foreign MNCs here to service domestic demand; Tesco’s is the biggest foreign employer in Ireland and its profit rate is higher in Ireland than anywhere else. Tesco’s is going nowhere. By contrast, the US Chambers of Commerce speaks increasingly for companies who have no activity and no employees in Ireland- apart from tax specialists - and who pay an effective rate as low as 1% or less.

Fiscal Impact

It has become common currency to quote a short OECD briefing paper as to the effects of FDI as if it were the last word on this issue. Unfortunately, for advocates of low taxes the note (based on a much larger study) suggests that the impact of a 1% hike in the corporate tax take is anywhere between 0% and 5% of total FDI. That is, according to the OECD higher taxes might have no impact at all on FDI.

Even the OECD’s central estimate is that a 1% hike in the tax rate would produce a fall of 3.7% in FDI. But what is the total impact on the fiscal position? According to a sketchy note from the DoF MNCs are responsible for 30% of corporate tax revenues. On 2010 tax returns that’s just under €1.2bn- yes, corporate taxes are under €4bn, compared to over €10bn from VAT and €11.3bn from income tax.

If the tax rate was hiked to 17.5%, on the OECD’s central estimate FDI would fall by 18.5%. On an extreme assumption that 18.5% of existing MNCs will flee as result (which no-one seriously suggests) then the remaining 81.5% of MNCs would then be paying 40% more in tax (the ratio between 17.5% and 12.5%), with a higher tax take of €1.37bn resulting.

Crucially, those eager to make the case for low taxes ignore entirely the increased tax revenue from the indigenous sector, which provides the remaining 70% or nearly €2.8bn of corporate taxes. The tax take from them would also rise by 40%, to €3.92bn. The combined total in corporate tax revenues from both MNCs and domestic sources is therefore just under €5.3bn, a rise of nearly €1.4bn. Of course, all these are taxes on profits which remain abundant in this economy, and by definition cannot be ‘unaffordable’.

Drivers of FDI

UNCTAD is the main international body providing detailed research on capital flows, doesn’t even mention tax rates as an important factor impacting FDI. In a survey of the literature a host of factors is considered, growth, market size, trade openness, ‘human capital’, infrastructure, political and economic stability, etc., etc. None mentioned tax.

Other research, dealing solely with the advanced economies such as Ireland, suggests not taxes but Total Factor Productivity as the main determinant of FDI (linked here). This is because TFP determines the total return on investment, not just the tax rate on that return. Plainly 12.5% tax on a 10% return on capital is a lower net profit than 39% taxes on a 15% return.

In fact, what the OECD’s longer research didn’t consider is that there is no zero bound to the effect on FDI from lower taxes- that the effect can be negative. This is borne out in a recent survey of FDI allocators for ‘Think London’ on foot of the Tory government’s announcement of cuts in corporate tax rates from 28% to 24% (the target since lowered again to 23%). The FT reported that its FDI Barometer survey found that that the net response was the investors were less likely to invest following the announcement of lower taxes (and they were also repelled by the government’s racist immigration policies).

These two points are related. Since TFP is actually the main determinant of FDI in advanced economies, it is the factors affecting TFP which determine its flow. Productivity derives from investment and the government component of that usually includes education, transport, communications, infrastructure, etc. Lower tax rates leads to lower tax revenues and a diminished capacity to invest in those areas. Declining relative productivity follows, deterring FDI, not encouraging it.

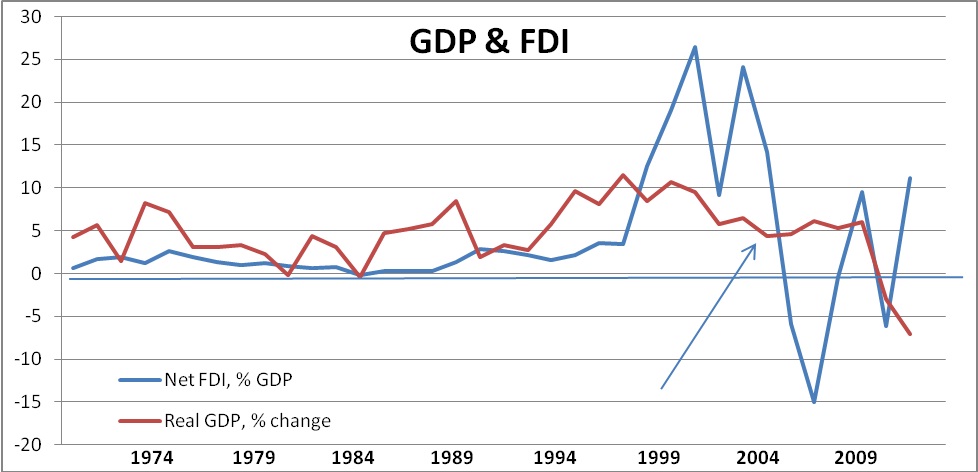

This is close to the experience in this economy. The chart below shows World Bank data for Irish real GDP and net FDI as a percentage of GDP.

12.5% tax rates were introduced in 2003. 2004 to 2006 saw outright falls in FDI, which also fell again in 2008. Including the surge in 2003, the annual average growth in FDI since is just 1.5% of GDP. From the time of the McCreevy 1998 Budget announcement average FDI net inflows have been substantially higher, but clearly that trend has gone into reverse.

The low-tax ‘Celtic Tiger’ actually saw much slower growth than the period that preceded it, even though it was widely claimed the reverse would happen – that lower taxes would lead to increased FDI and higher growth. GDP growth peaked at 11.5% in 1997 - the year before the announcement of lower taxes was made. It has been less than a third of that rate since 2000.

Lower taxes produce lower tax revenues, lower growth and lower FDI. They do produce higher post-tax returns on capital – but that’s not an argument for maintaining them. The two EU countries with the highest post-tax returns on capital are Greece, followed by Ireland. This is a source of economic weakness, not strength.

Share:

![Duggan, Vic]](/assets/img/2017/04/1491994913319631_sq.jpg)