Public Spending

By understanding how public money is raised and spent – and matching it to government policy – we can work out what the government’s priorities are, and how they relate to what is important to us.

This guide outlines how the public finances work.

This includes details about the annual Budget, which sets out the government’s programme for public spending and taxation for the year ahead.

PDF version of the guide

PDF version of the guideFind on this page

Public finances - money in, money out

One of the most important roles of any government is to manage the public finances. This involves making decisions on raising and spending public money.

The public finances can be broken down and understood in different ways. But there are always two essential components: money that is raised and money that is spent.

- Public revenue: This is money the government raises, mainly from taxes, like income tax and levies on goods and services. There are also other sources, for example surplus income from commercial semi-state companies.

- Public spending: This is also referred to as public expenditure. It is the taxpayers’ money (plus State borrowings) that the government spends. Public spending is limited by the amount of revenue available to the government and the size of the public debt.

Both public revenue and public expenditure are often discussed in cash terms. But they can both also be expressed as a percentage of the overall economy, or Gross Domestic Product (GDP) .

Two types of public spending

There are two types of public spending. They are:

Current or day-to-day spending: This includes salaries for teachers, nurses and other public servants; and

Capital or investment spending: This includes spending on public infrastructure like the Luas light rail system in Dublin, and buildings such as schools and hospitals.

How governments raise revenue

There are two main categories of taxes: direct taxes and indirect taxes.

Direct taxes

These include income tax and the Universal Social Charge (USC) which is payable on gross income, i.e. before income tax is deducted.

Pay Related Social Insurance (PRSI or Social Insurance) is often counted alongside income tax as part of the total taxes on paid work.

However, it is not technically a tax, and is designed more as an insurance premium. It does not go into the government’s central tax fund, but instead is paid into the Social Insurance Fund.

This money is then used to pay certain benefits like state pensions or illness benefits. This fund is sometimes referred to as part of the 'social safety net'.

Indirect taxes

These include 'consumption taxes,' based on things we buy as consumers, such as Value Added Tax (VAT) which is levied on goods and services.

Excise duties, which are paid on goods like alcohol, cigarettes and fuel, are another form of consumption tax.

Other indirect taxes are: taxes on property (the Local Property Tax); taxes on capital (like inheritance tax or gift tax); and corporation tax (a levy on companies’ profits).

Income tax and VAT are generally the two main sources of public revenue raised by the Irish government each year. For example, in 2014 these two sources accounted for almost two thirds of all tax revenue,according to figures from the Revenue Commissioners.

Collapse of tax revenue post financial crisis

After the financial crash of 2008, tax revenue in Ireland collapsed. This included reductions in:

- income tax as people lost their jobs

- taxes on sales and purchase of property as the property market collapsed

- corporation tax as companies lost profits

- VAT as people stopped consuming so much and sales of goods and services went down

At the same time, social welfare payments had to increase to meet the demand from growing numbers of people who had become unemployed. The result was that the amount needed for public spending exceeded the amount of public revenue raised.

We are all tax payers

Everyone is a tax payer. Most people at work, whether full-time or part-time, pay taxes on income (those on low incomes don’t). Some people in receipt of social welfare payments, like pensioners, also pay income tax. And as consumers, the full population of 4.61 million pays taxes on goods and services.

Progressive and regressive taxes

Taxes can be progressive or regressive.

Progressive taxes are those that increase as a percentage of gross income, as incomes rise. Income tax is technically a progressive tax because the rate progresses upwards, with someone on a higher income paying some of their taxes at a higher rate meaning that they pay proportionately more.

Regressive taxes are those that take a greater proportion of income from low earners as opposed to high income earners.

For example, VAT is generally considered a regressive form of taxation. This is because the same amount must be paid by everyone, regardless of their income level. The result is that lower earners pay a higher percentage of their overall income in VAT than higher earners.

Redistribution through taxation

Redistribution is a central role of the tax and benefit system. Progressive taxes are used to redistribute economic benefits across society, for example, to fund the education and health systems.

Government borrowing

Typically, it sells government bonds, in which it promises to pay back the face value of the bond plus interest by a certain date.

Since 2008, Ireland has also had to borrow substantial amounts of money from the European Central Bank, EU Commission and the International Monetary Fund. This was because the banking and economic crisis led to a huge expansion in the country’s national or sovereign debt.Some, but not all, of this debt was a direct result of the government’s move to ‘bail out’ privately owned banks.

How public money is spent

Every year, the single largest chunk of government spending goes to social protection, including disability and unemployment supports and pensions. The main purpose of these payments is to provide a safety net so that individuals and families do not fall below a minimum standard of living.

This also includes child benefit which is paid for every child regardless of the income of the parent(s) and is an important contribution to the support of children and the reduction of 'poverty traps'.

Funding for public services is the second largest category of public spending. These services include health, education, local government, defence and the salaries of civil and public servants, like government officials, nurses, doctors, teachers, social workers and gardai.

Investment in economic and social infrastructure to support private enterprise and economic activity and enhance the quality of life of all citizens is the third main category of public spending each year.

This would include funding to attract business investments, improve transport networks, develop agriculture and tourism, and protect consumers.

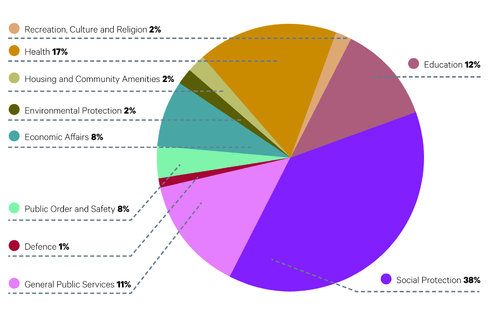

How €69.8 billion in public money was spent in 2012 (source: Eurostat, 2012)

The piechart below gives a breakdown of how the government spent almost €70 billion in public money in 2012. It shows that the ‘big three’ spending areas are social protection, health, and education.

- €7,036 on health services

- €5,155 on education

- €780 on cultural and recreational activities

- €163 on fire protection services

The category labelled in the pie chart ‘general public services’ includes interest repayments on Ireland’s national debt.

Note about the pie chart

While there are more up to date figures on government spending, the pie chart shows spending across the ten 'functions of government'. This is a standard UN classification that allows public spending in a country to be compared over time, and also to be compared with public spending in other countries.

Links between private sector and public sector

The private sector and the public sector are closely linked and mutually dependent.

The private sector relies on the quality of publically-funded infrastructure such as roads and internet broadband, as well as education and health services, training, public transport and other services. All of these create an environment in which private business can thrive.

The public sector purchases goods and services from the private and not-for-profit sectors.

The government also supports employers and the self-employed in a variety of ways. For example:

- State assistance is provided to businesses from Enterprise Ireland, the Industrial Development Authority and County Enterprise Boards.

- The farming and fishing industries also receive direct government help via subsidised diesel fuel.

- Farmers and fishermen receive direct payments from the European Union's Common Agricultural Policy and Common Fisheries Policy. These are paid for by the taxpayers of all EU Member States, including Ireland, by the transfer of a proportion of national VAT receipts to the European Union.

GDP and why it is important

Gross Domestic Product is the main measure of the size of an economy. It is the total value of all goods and services produced by the economy in a period. This includes government services, consumption by individuals, investment by businesses, and trade (imports and exports).

Put simply, when a country’s GDP goes up, the economy is growing. When it goes down, the economy is contracting. Two or more consecutive quarters of contraction means the economy is officially in recession. Ireland's GDP is measured by the Central Statistics Office every three months.

There is an ongoing debate about the validity of measuring the wealth of the country in this way. Many argue for an alternative measurement which would include for example the contribution made by unpaid care-giving.

Also, while GDP is the standard measure of economic growth, an alternative measure is Gross National Product (GNP). GNP strips out the effects of profit flows to foreign-owned companies which do not contribute to the Irish economy. The total income remaining with Irish residents and companies is the GNP. Because of the large number of foreign multinationals based in Ireland, there is a significant difference between GDP and GNP.

Find on this page

The annual Budget

Every year, the government sets out its plans to both raise and spend public money for the year ahead. It does this in the annual Budget.

The Budget is the clearest statement we have about the government’s priorities and policy commitments.

If you want to fully understand government thinking in a particular area, you can do this by familiarising yourself with the parts of the Budget relevant to it.

The Budget is announced by the Finance Minister and the Minister for Public Expenditure in October. The Department of Finance generally publishes fact sheets on Budget day on its website.

These set out the main changes and how they will affect individuals and families. Newspapers and other media outlets are also a good source of easy to understand Budget analysis.

What influences Budget decisions?

There are many factors that governments must take into account when planning the Budget. These include:

- The size of the national debt – public money must be set aside to service this. If more tax revenue is spent servicing debt, there is less available for public spending, for example on health and education services and pensions.

- The age of the population – this will determine how much public money must be spent in areas such as education, healthcare and state pensions. In Ireland, the share of the population aged 65 years and over is growing. Currently however there is a reasonable balance between those of working age, children and elderly.

- The state of the economy – Budgets can be used to stimulate the economy in certain ways. Public spending can also be withheld to avoid creating an economic ‘bubble’.

- One-off factors – like whether there have been any natural disasters that require the government to spend money, or claims for compensation arising from political or administrative negligence or errors in the past.

- Programme for Government commitments – a government's work plan may set out particular economic policies or priorities for its term in office

- The influence of interest groups – including trade unions, employers, business bodies, farmers, civil society groups, etc. Different groups have different degrees of influence.

The Budget contains tax and spend changes

Government resources are always limited. It is the annual Budget that determines who are the ‘winners and losers’ in public spending, and which sectors of society benefit most. Changes announced in the Budget in any given year are likely to affect our take-home pay, the amount of money we spend on goods like alcohol and diesel/petrol, and the quality of the public services available to us.

Budgets usually include changes to:

- tax rates and bands including income tax (taxes can go up or down)

- rates of social welfare payments including child benefit

- tax ‘relief’ measures to encourage people to invest in certain areas

- the amount of money available for ‘capital’ projects - for example to build new houses or schools

- government programmes or services - for example in health or education

Budgets as politics

Exactly how they do this depends on their political beliefs about how and from whom public funds should be raised, the kinds of public goods and services that should be provided as public services, and how these should be paid for.

For example, in Ireland public transport is partly subsidised by public money, while users are also charged fares, (unless one qualifies for free transport as a recipient of certain social protection payments).

In other countries public transport is more heavily subsidised through taxation, with the result that fares are cheaper. The degree to which a government chooses to subsidise public transport in this way often boils down to a question of political ideology - and the public’s willingness to accept higher rates of direct or indirect taxation).

Issues that affect budget choices

Some Budget choices are based on technical considerations or government commitments that must be met – like paying down national debts.

But many others are the result of trade-offs between the best technical solutions (or the least-worst options) and the reality of politics and various interests within the country.

Many groups and individuals try to influence the content of the annual Budget. These include government Ministers, department officials, business groups and economic lobbies, trade unions, charities and non-profit groups. Many of these groups have competing or even conflicting priorities and demands.

While budgetary policy is decided nationally, as a member of the European Union Ireland must observe some overall rules set at EU level.

Budget day – part of an annual cycle

Budget Day is only one part of the continuous cycle of economic planning that governments undertake. The exact date of Budget Day is not fixed – currently it takes place in mid-October.

This is when the Budget documents (called the Financial Statement and the Estimates Statement) are formally presented to Dáil Eireann, the lower chamber of the Houses of the Oireachtas.

The bulk of the planning and preparatory work for the Budget takes place much earlier in the year. The broad framework about cuts or increases in spending or tax to be contained in the Budget is decided in the summer, about three months ahead of Budget Day.

However, important or politically sensitive measures may not be agreed by the government until very close to Budget Day itself.

Budget timeline by season

Here is a season-by-season guide to how the annual Budget is planned and executed:

Spring: Budget planning gets underway in earnest

Officials and Ministers begin preparing for the October Budget in earnest before Spring.

In April the Department of Finance publishes the first official economic forecast that the government will have produced since the previous year’s budget.

This is called the Stability Programme Update (SPU) and it is an EU requirement – all EU states must lay out their fiscal plans each April as part of the EU’s economic governance rules in the Stability and Growth Pact.

The SPU outlines in very broad terms how much money the government thinks it will raise and spend in the coming years.

The SPU may be accompanied by a Spring Economic Statement from the Minister for Finance and the Minister for Public Expenditure and Reform. This sets out the key parameters and economic underpinnings of the Budget position. The first Spring Economic Statement was issued in April 2015.

Around this time the Tax Strategy Group is set up for the year ahead. It is an inter-departmental advisory committee which examines budgetary proposals related to tax, social welfare and PRSI. It is set up afresh for each Budgetary cycle.

Summer: Meetings between finance officials and government departments

Over the summer, officials in the two key financial departments – Finance, and Public Expenditure – start to work on the Budget arithmetic in detail. The Department of Finance develops tax measures, while the Department of Public Expenditure develops expenditure measures.

On the expenditure side, discussions take place with government Ministers and departments, based on each department’s ‘expenditure ceiling’. This is a Department of Finance/Public Expenditure cap on the amount of money each department is allowed to spend in the coming year.

These ceilings are set every year as part of what are called the Estimates – detailed reports on how each department will spend its money. The ceilings can be modified only in extreme circumstances.

The spending projections in the Estimates do not vary much from year to year. This is because it costs more or less the same amount of money every year to run each government department and the various public agencies that they fund.

However, there can be significant fluctuations in spending at department level, for example if there has been a government decision to increase or decrease expenditure in any given area. Also, the spending of the Department of Social Protection is directly affected by unemployment rates either rising or falling.

While the Estimates themselves do not take into account any new policy measures, they provide the government with a strong idea of how much scope it has for the forthcoming Budget’s spending and revenue-raising measures.

Summer: Pre-Budget submissions from interest groups

In June, a ‘Budget memorandum’ goes to government (the Cabinet) for approval. This sets out the broad framework for the forthcoming October Budget.

In the months directly leading up to Budget Day, hundreds of organisations and interest groups publish and submit ‘pre-Budget submissions’ to the government. These are formal documents which generally call for spending increases or tax reductions for the people, sectors or organisations the groups represent.

The Oireachtas Finance Committee holds hearings with interested groups and individuals and sends a summary report on these to the Minister for Finance. These proposals are weighed up by officials and Ministers in deciding how to structure their proposals for the year ahead.

In July 2015, a new formal public consultation process was introduced. The National Economic Dialogue was a two-day event at which invited stakeholders discussed their Budget priorities with government Ministers.

Autumn: The Estimates are published

The Estimates of Receipts and Expenditure for each department (calculated on the basis of no change to taxation) are presented to the Dáil about a week before Budget Day.

They are the government’s opening position for the Budget to come. They are formally known as the ‘White Paper on Receipts and Expenditure’. They show where the government is planning to spend its current income in the coming year. This gives a base from which to compare the changes to be announced in the Budget.

The Estimates are essentially a technical pre-Budget document.

They do not include any new policy measures to be included as part of the Budget, such as changes to tax rates or new spending initiatives.

Mid-October: Budget Day

On Budget Day, the main Budget measures – the increases or decreases in taxation or spending – are outlined in speeches to the Dáil by the ministers responsible for the public finances.

The Minister for Finance outlines the main tax or revenue-raising measures. The Minister for Public Expenditure and Reform sets out the main spending measures.

Much greater detail of these are contained in a separate document, the Comprehensive Expenditure Report, which is also released on Budget Day.

Winter: Budget changes are voted through the Dáil

Before any Budget measure can take legal affect, the Dáil has to vote it through. Given that governments rule with majorities, this process is generally a formality.

Budget changes that are due to come into force immediately – like increases in duties on alcohol or petrol – must be voted through on Budget Day itself. This is done by passing financial legislation, known as Financial Resolutions, on each particular measure.

The remainder of the Budget changes that must be introduced in primary legislation (an Act of the Oireachtas) are included in two separate Bills published soon after Budget Day. These are:

- the Finance Bill, which gives legal effect to the Budget’s tax measures; and

- the Social Welfare Bill, which provides for changes to social welfare payments.

These Bills are generally published in late October or early November, becoming Acts of the Oireachtas before the end of the year.

Budget changes can be introduced after Budget Day

Budget Day announcements are not set in stone. The Finance Bill and Social Welfare Bill generally include measures that were not announced on Budget Day itself. These could include entirely new measures or changes to measures as announced.

Sometimes significant changes are made between the Budget Day announcement and the introduction in the Dáil of the Finance Bill and the Social Welfare Bill.

These may be due to technical reasons, new Budget allocations that emerge, or lobbying by interest groups.

Winter: the Revised Estimates are published

The Budget cycle does not end until the publication of what are called the Revised Estimates for Public Services, or the Revs. These usually contain allocations for spending in key areas that were not already announced in the Budget.

The reason for this is largely technical: the Budget comes out before the formal tax year ends. This means that the Budget arithmetic is based only on government estimates of how much tax income it has to spend.

When the actual figures of the amount of tax paid in the tax year emerge, they may show that the tax take was higher than envisaged. If this is the case, it means the government has more money to spend.

The excess amount is generally distributed to fund particular areas or causes, and these allocations are reflected in the Revs. The Revs also include the departmental expenditure ceilings for the following year, which form the starting point for expenditure costings in the next Budget cycle.

Spending can also vary in any given Department in the course of year, but this has to be agreed by government.

Budget rituals and secrecy

Budget Day comes with a lot of ritual and is intensely watched by the public, media, interest groups, business and trade unions, and the financial markets.

Traditionally, the details of the Budget are kept secret until they are announced in the Dáil.

The Budget document itself is only circulated to parliamentarians in the Dáil chamber once the Minister for Finance begins speaking. For some budget measures such secrecy is necessary; for example in relation to some taxation measures, in order to avoid giving advantage to some taxpayers over others. Nevertheless most Budget announcements are kept secret in order to enhance their political impact as part of a bigger package.

Accentuating the positive

It is often the case also that some negative aspects of the Budget are not revealed in the Budget Dáil statements. Sometimes these appear only in the more detailed Comprehensive Expenditure Report which is published alongside the Budget.

Sometimes, Budget changes may only become obvious when the Social Protection Bill and Finance Bill are tabled – these two pieces of legislation are required to give legal effect to key measures announced on Budget Day.

The downside of Budgetary secrecy is that elected representatives have little opportunity to hold the government to account when it comes to significant public spending decisions included in the Budget.

A striking example of Budget secrecy was the 2003 Budget Day announcement to decentralise government departments by moving 10,300 civil and public servants from Dublin to 53 locations in 25 counties.

The decentralisation plan was subsequently cancelled as it was largely impractical.

Find on this page

Influencing the Budget

There are many reasons why you might want to seek to influence public spending and the Budget itself.

You could be a citizen who is curious about how your tax money is spent and the government’s spending priorities. Or you may be an activist or campaigner who wants to make a case for increased spending in a particular area.

The section of the guide outlines key ways for groups or individuals to try to make a case for Budget changes. The Toolkit Guides to Policy Making and Law-Making also have more general information on how policies and laws are made and how to influence them.

Get to work early in the Budget cycle

It important to start early in making your case with key decision-makers and decision influencers. These include government Ministers and their special advisers, national and local politicians, senior civil servants (usually Principal Officer level and above) and media outlets.

Final decisions about government spending are taken by Ministers, often in close consultation with their political advisers. They are acutely aware of the sensitivities of voters and are keen to avoid stepping on any Budget ‘banana-skins’. There are several formal channels for groups or individuals to seek to influence the Budget. These are:

Prepare a pre-Budget submission

Many groups and organisations take the formal route of making a ‘pre-Budget submission’ to Ministers and others setting out their Budget priorities.

Making a strong submission involves research and may also require some familiarity with economic data. However, if you lack expertise in public finances, you should not let that discourage you from making a submission. It is also possible for an individual or group of citizens to simply write a letter to a Minister outlining a change that they would like to see.

Before deciding whether to make a pre-Budget submission, you should ask yourself:

- What do you want to achieve by making a submission?

- Is making a pre-Budget submission the best way to achieve the change you want to see, or would campaigning and media work be more effective?

- Does your organisation have the resources to put together a compelling submission and to advocate and lobby around it?

- Can you collaborate with any other groups on your pre-Budget submission, particularly those that are well resourced and have technical expertise?

Tips for making a pre-Budget submission

- Keep your submission short and simple. Decide what your key priorities are and argue the case strongly for these. A tight and focused Budget submission is better than a long shopping list.

- Where possible, include sound evidence and even financial costings for your Budget proposals, if you can manage. It is also a good idea to estimate any savings in public spending that your Budget proposals would produce.Government departments may be a resource here as they often supply current costings, for example in response to Parliamentary Questions, which you can ask a TD to submit.

- Include real life examples like case studies or real stories from your experience or people affected by the problem you want to see addressed.

- Demonstrate the ‘public value’ of your argument. Ministers and civil servants can be influenced if it can be shown that the issue affects significant numbers, or even small numbers if there is a genuine injustice involved.

- If you can, show how your proposals fit with existing government policies or priorities. If you can demonstrate how your submission dovetails with a department’s current strategy you will stand a better chance of succes. Alternatively, you might set out to show in your submission that current policy is mistaken and should be changed.

- Send your submission to both the Minister for Finance and the office of the Minister responsible for the area you are interested in. In each case you should request that the issue you raise be added to the Tax Strategy Group’s agenda for consideration. This is an inter-departmental advisory committee which examines budgetary proposals related to tax, social welfare and PRSI. It is set up afresh for each Budgetary cycle. (Read more about the Tax Strategy Group.)

- It can be beneficial to also send your submission to Ministerial advisers and civil servants in the department responsible for your issue. You can find who these individuals are by telephoning the department or checking on its website.

- Circulate your submission to all TDs, Senators, Oireachtas committee chairs, opposition spokespeople for the issue, and the media.

Budget submission by health group calculates cost savings

In its pre-Budget submission calling for a 20 per cent tax on sugar-sweetened drinks in Budget 2014, the Irish Heart Foundation calculated that the tax would generate about €60million for the Exchequer. It also estimated that it would reduce the €1.13 billion that obesity costs the State each year.

Attend Budget Forums

The Minister for Social Protection hosts an annual Pre-Budget Forum where community and voluntary groups can present and share their ideas. Only groups who are invited can attend this day-long event. The forum gives the groups an opportunity to present their proposals directly to the Minister and his or her officials. See the attendees for the 2015 Pre-Budget Forum.

A separate formal government consultation called the National Economic Dialogue took place for the first time in July 2015. This two-day event allowed a range of invited interest groups and stakeholders to discuss Budget options.

Use the Budget ‘build up’ for campaigning and networking

Many groups view the pre-Budget period as an important part of their broader campaigning efforts to put their issues on the political agenda. They may use it as an opportunity to seek media coverage for their causes in order to build public pressure and support.

Even if your Budget submission is not successful, the pre-Budget period may offer you a good opportunity to seek meetings with Ministers, public representatives and key officials involved in the policy-making process. Ahead of meetings, you should rehearse your pitch and prepare answers to any obvious counter-arguments that you might face.

It is always a good idea to build alliances with other groups, if possible. This means you can share the workload in terms of lobbying, networking and media work. Also by having a common platform with other groups you will strengthen your case with policy-makers.

Some business interest groups and non-profit organisations, including think tanks and charities, produce pre-and post-Budget analysis documents containing useful research that other groups can use to support their arguments.

Find on this page

Budget decision U-turn - lone parent group's efforts to block cuts to poorest households

A planned Budget 2015 cut to welfare payments for working single parents was successfully reversed following intense lobbying by groups representing one-parent families.

The last minute Budget reversal benefited some 28,000 of the poorest households with children, while staying within the Budget allocation for the Department of Social Protection for 2015.

Here Stuart Duffin (on right of the photograph above), director of policy and programmes at the lone-parent organisation One Family, explains how the organisation used its knowledge of the Budget and policy-making process to push for the change:

Problem identified

“Anyone receiving One Parent Family Payment who gets a job can earn up to €90 a week and also keep their full welfare payment of €188 per week.

This is because the first €90 of a person’s weekly earning is disregarded when it comes to assessing whether they qualify for the full One Parent Family Payment. The idea behind this 'income disregard’ system is that it provides a safety net that encourages and supports lone parents to get out of poverty and into the workplace.

In 2011, the amount of income that was disregarded for people receiving One Parent Family Payment was €146.50. It was announced in Budget 2012 that the disregard would be reduced each year in successive Budgets until it was €60. Budget 2015 was supposed to reduce the income disregard from the current rate of €90 a week to €60.

Putting knowledge of the Budget process to work

“When we saw on Budget Day that the reduction was still planned, we set out to reverse the decision. We realised that this was a political decision that could not be solved just by talking to officials in the Department of Social Protection. So we focused on trying to influence the Minister for Social Protection, both directly and through Ministerial advisers and backbench TDs from the Minister’s party.

We knew we only had a few weeks to get the change we wanted before the Social Welfare Bill was introduced, as it turns the announced Budget measures into law. We wrote to the Minister directly appealing for the income disregard to be maintained at the rate of €90 a week. We pointed to a mass of international evidence that shows that income disregards really help lone parents move into work.

Making the case for no Budget changes

"We also pointed out that through our social media feedback and our work with clients that the rhetoric of ‘work pays’ was fast becoming an untruth for many one-parent families. The lived reality was that people were telling us that they were considering having to give up work if the planned cut was put in place, because it wouldn’t be worth their while.

We calculated that maintaining the income disregard at €90 would cost €8.3 million in 2015. In the context of a Social Protection Budget of more than €19 billion, this was a modest proposal. In the end, the policy-reversal was funded from within the department’s existing allocation for 2015.

Minister gets the message

The Minister took our message on board and got government approval to keep the income disregard at the current level of €90. She announced this when she brought the Social Welfare Bill to the Dáil for parliamentary approval of social welfare changes in Budget 2015. The Minister introduced an amendment to the Social Welfare Bill that reversed the cut that had been originally outlined in Budget 2012.

Advice to others seeking Budget changes/changes to public spending:

“If you want to see change you have to be solution-focused, based on lived experience and evidence-informed. The policy process is often not pretty, and it can be messy. Yet advocacy efforts need to understand how the policy process works and where you are likely to find success and to describe what success looks like for policy formers and makers. Workable policy solutions are achieved through the convergence of problems, proposals and politics."

Read more:

- Official announcement by the Minister for Social Protection that the income disregard for the One Parent Family Payment would be kept at its current level of €90 a week.

- One Family – Ireland’s organisation for people parenting alone and sharing parenting – welcomed the announcement.

- The Minister’s amendment to the Social Welfare Bill 2014 keeping the income disregard for the One Parent Family Payment at the existing level.

Information on the Budget and public spending in Ireland

The main Budget statements and background documents are published on the website www.budget.gov.ie.

Further details of Budget measures are also available on the websites of the government departments affected by the changes.

Comprehensive Expenditure Report

A key Budget document is the Comprehensive Expenditure Report 2015-2017.

This sets out the details of expenditure in all areas of government for the year 2015, as well as proposed expenditure for 2016- 2017. It also explains what public services will be delivered in 2015 for the money allocated.

The report breaks down spending into about 42 headings, which are listed as (Dáil) ‘votes’ because the Dáil has to vote on them as part of the annual Budgetary process.

These represent the main spending programmes for each government department and the public agencies that they fund.

The estimated expenditure is broken down into two parts: ‘capital’ spending, which would include once-off spending on infrastructure and buildings; and ‘current’ spending which covers day-to-day costs like salaries.

The Comprehensive Expenditure Report is not a full picture of government spending in a given year. This is primarily because it does not include details of non-voted expenditure.

This is money that government departments get from other sources that are not voted on by the Dáil, from sources like the National Lottery Fund or the Environmental Fund which is funded by the plastic bag tax.

Exchequer Statements

Exchequer Statements are produced at the end of every month. They show all receipts (revenue) and expenditure from the 1st of January to the end of each month. They also include a comparison with the same time period for the previous year.

Eurostat

Eurostat is the European Commission’s statistical agency. Its detailed database provides standardised statistics at European level that enable comparisons between countries and regions.

For example, Eurostat publishes statistical data on how much each of the 27 European Union countries spend on public services. These are measured under ten standardised headings called General Government Expenditure by Function (COFOG).

Budget analysis

- The Citizens Information Board publishes an annual summary of the key Budget changes, as well as annual pre-Budget submissions.

- Non-profit groups including Barnardos, TASC, the Nevin Economic Research Institute, and Social Justice Ireland all publish budget submissions or analysis.

- The Economic and Social Research Institute publishes an annual ‘distribution analysis’ of how the Budget affects different groups in society.

- Interest groups and the main trade unions also publish analyses of how the Budget affects their members.

- The main accounting firms and business representative bodies also publish Budget submissions and responses.

Data on public revenue - taxation

- Tax Strategy Group papers

The Tax Strategy Group assists the Department of Finance in making its Budget decisions. This is an inter-departmental committee chaired by the Department of Finance. A key role is to examine and develop proposals for tax, social welfare and PRSI, and look at how the various proposals interact with each other and how they will affect the economy.

- Revenue Data

Revenue data is the key source of statistical information on what is happening in the economy, how much people are earning and paying in tax, how much government revenue is coming from sales or property transactions and business profits. It contains detailed statistical information on taxes and duties including:

- Receipts – tax take – by tax group (VAT, Income Tax, Property Tax)

- Ready Reckoners – explain – a table which outlines the cost of tax cuts or the revenue raised by tax increases

- Registrations, Assessment and Transactions

- Income Tax and Corporation Tax

- Vehicle Registration Tax

- Incidence of Excise and VAT on Oils, Alcohol and Tobacco

- Cross Border Price Surveys

- Local Property Tax Compliance Stats

- Revenue Statistical Reports 1996-2012 (discontinued)

- Tax Trends in the EU

The Taxation Trends in the EU report contains a detailed statistical and economic analysis of the tax systems of the Member States of the European Union, plus Iceland and Norway, which are Members of the European Economic Area. It is useful for comparing tax systems.

It offers a breakdown of tax revenues by economic function (i.e. according to whether they are raised on consumption, labour or capital). Besides revenue data, the report also contains indicators of the average effective tax rate falling on consumption, labour and capital, as well as data on environmental and property taxation and on the top rates for the personal and corporate income tax.

Country chapters give an overview of the tax system in each of the 30 countries covered, the revenue trends and the main recent policy changes.